The Northeastern United States is once again grappling with tightened heating fuel supplies, prompting an extension of emergency trucking waivers. This development, rooted in an ongoing outage at Energy Transfer LP’s Marcus Hook terminal and compounded by impending winter weather, underscores the fragile balance of regional energy logistics. While the immediate impact on consumer prices has been contained, the situation highlights critical vulnerabilities within the supply chain for propane, natural gas, and heating oil, demanding keen attention from investors assessing the resilience and profitability of energy infrastructure in a dynamic market environment.

Northeast Heating Fuels Under Pressure: A Deeper Dive into Regional Vulnerabilities

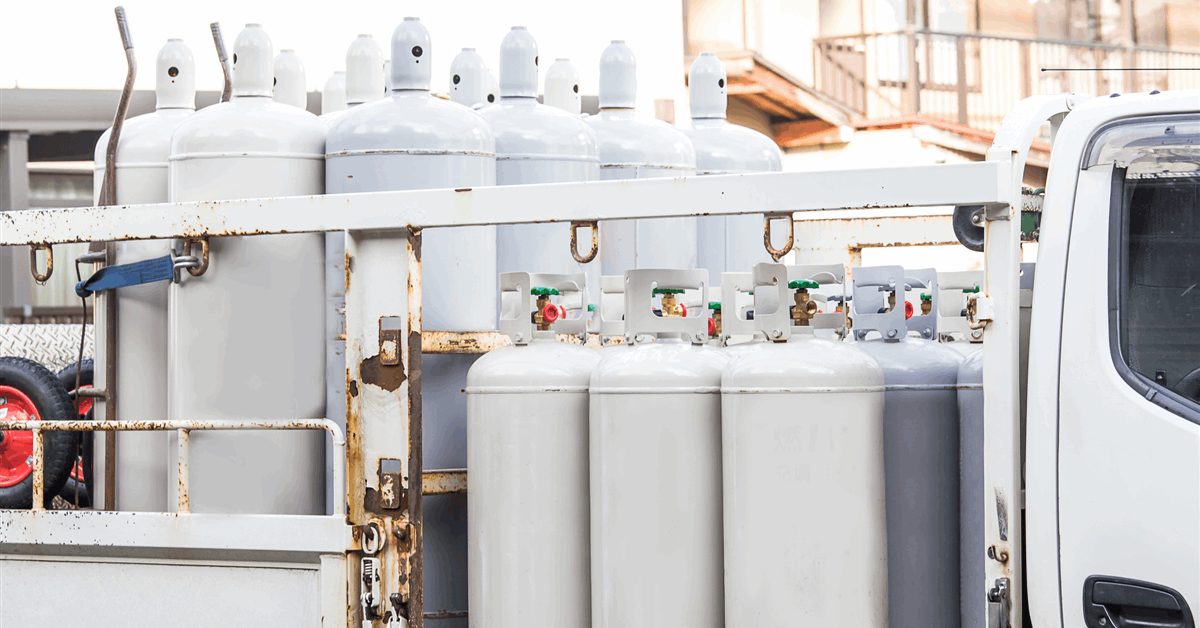

The Federal Motor Carrier Safety Administration has extended its emergency declaration through January 15th, waiving crucial regulations on driver hours to ensure continuous distribution of heating fuels across the Northeast. This measure, initially enacted on December 12th for New York, New Jersey, Delaware, and Pennsylvania, has now expanded its scope to include Connecticut, Maryland, Massachusetts, New Hampshire, and West Virginia. The core of the problem traces back to a November 19th electrical incident at Energy Transfer LP’s Marcus Hook terminal in Pennsylvania, which disabled the facility’s ability to load propane onto trucks for three days. The resulting force majeure declaration placed Energy Transfer’s customers on allocation, reportedly receiving only 70% of their contracted loads.

Despite this significant disruption, the immediate fallout for consumers and prices has been mitigated. East Coast propane inventories are currently in line with prior-year levels, and retail prices in the region have seen only a modest increase of approximately 5 cents since the outage began. This resilience can be attributed to existing fuel stockpiles and distributors’ ability to source propane from alternative plants. However, the forecast introduces new challenges: a fast-moving storm, the “Alberta Clipper,” is set to bring freezing air into the Northeast and mid-Atlantic states this Friday, with New York City and surrounding areas potentially seeing 4 to 8 inches of snow. Another shot of cold air is anticipated next week, further stressing the logistics network and potentially testing the limits of current inventory management strategies for essential heating fuels.

Broader Market Context: Crude’s Downtrend Amidst Localized Supply Shocks

While regional heating fuel markets navigate these localized supply challenges, the broader crude oil complex presents a contrasting picture. As of today, Brent crude trades at $90.03 per barrel, experiencing a modest 0.44% decline for the day, with its intra-day range spanning $93.87 to $95.69. WTI crude follows a similar trajectory, currently at $86.32 per barrel, down 1.26% today, trading between $85.50 and $87.47. These figures indicate a relatively stable, albeit slightly downward, daily movement. However, zoom out, and the trend becomes starker: Brent crude has shed a significant $23.49, or nearly 19.8%, from its recent peak of $118.35 on March 31st to $94.86 just yesterday. Gasoline prices are also seeing a slight dip today, trading at $3.03 per gallon.

This overall downtrend in crude prices provides a complex backdrop for investors. On one hand, lower crude prices could theoretically ease some cost pressures on refined products like heating oil, offering a buffer against supply chain disruptions. On the other hand, the localized nature of the Northeast emergency highlights that even in a well-supplied or declining crude market, specific regional infrastructure failures or weather events can create acute shortages and price volatility for particular products. Investors must discern between macro commodity trends and micro-market dynamics, recognizing that companies involved in last-mile distribution, storage, and alternative sourcing for heating fuels might face distinct pressures and opportunities, irrespective of headline crude prices.

Upcoming Catalysts and Investor Sentiment: Navigating Uncertainty

The coming weeks are packed with pivotal energy events that will shape the broader market, influencing investor strategies beyond the immediate Northeast emergency. Our proprietary reader intent data reveals a common thread among investors: a desire to understand whether “WTI is going up or down” and to predict “the price of oil per barrel by end of 2026.” These questions underscore a prevailing uncertainty about market direction, which will be heavily influenced by several key dates on the calendar.

Tomorrow, April 21st, the OPEC+ JMMC Meeting is scheduled, a critical gathering that could signal shifts in production policy and significantly impact global supply expectations. Following this, the EIA Weekly Petroleum Status Report on April 22nd will offer crucial insights into U.S. crude, gasoline, and distillate inventories, including heating oil. The Baker Hughes Rig Count on April 24th will provide a pulse check on drilling activity, while subsequent API and EIA reports on April 28th and 29th, respectively, will continue to update inventory levels. A particularly important release will be the EIA Short-Term Energy Outlook on May 2nd, which will offer updated forecasts for supply, demand, and prices across various energy commodities. For investors tracking the Northeast situation, these EIA reports will be crucial for gauging heating oil and propane inventory health nationally and regionally. The interplay between these macro-level data points and the localized supply constraints in the Northeast creates a complex environment, demanding a nuanced investment approach that considers both global supply-demand fundamentals and regional logistical resilience.

Investment Implications: Beyond the Headlines

For discerning oil and gas investors, the Northeast energy emergency, while regional, offers valuable lessons and potential avenues for strategic positioning. It highlights the critical importance of a robust and adaptable energy infrastructure, particularly for midstream companies involved in the transportation, storage, and distribution of refined products like propane and heating oil. Companies with diversified sourcing capabilities and agile logistics networks are better positioned to weather such localized disruptions, potentially gaining market share from less resilient competitors.

Furthermore, the event underscores the enduring impact of weather on energy demand and supply chains. Investors should evaluate companies based not only on their production capacity but also on their operational resilience in extreme weather conditions. Given that East Coast propane inventories are holding steady, this suggests that the broader supply chain has some inherent shock absorption capacity, yet the pressure on trucking logistics remains a bottleneck. This could point to investment opportunities in trucking and logistics firms specializing in hazardous materials or those investing in alternative transportation methods. Ultimately, while the immediate crisis is being managed, the recurring nature of these challenges reinforces the need for a long-term investment perspective that prioritizes energy security, infrastructure resilience, and efficient supply chain management in the face of both operational incidents and increasingly unpredictable weather patterns.