In a significant signal for the offshore energy sector, TGS has secured a three-year extension for its ongoing ocean bottom node (OBN) seismic acquisition contract in the US Gulf of Mexico. This proprietary program, executed in partnership with a major operator, underscores a strategic commitment to enhancing reservoir characterization and optimizing production from existing assets. For investors, this move is more than just a contract renewal; it’s a window into how leading energy companies are navigating market volatility and long-term energy transition narratives, prioritizing efficiency and maximizing returns from proven resources. Through OilMarketCap’s proprietary data pipelines, we can dissect the broader implications of this extension, weaving together live market data, upcoming calendar events, and direct investor sentiment to provide a comprehensive analysis that goes beyond the headlines.

Deepwater Resilience Amidst Market Fluctuations

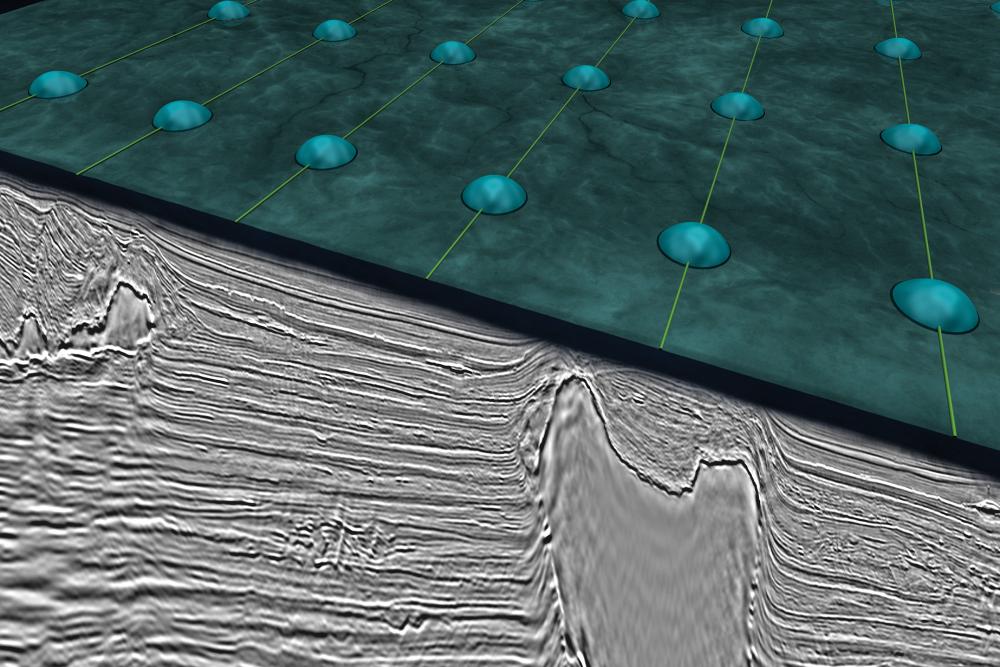

The decision by a major operator to extend TGS’s OBN seismic contract for another three years in the US Gulf of Mexico is a powerful testament to the enduring strategic importance of deepwater assets. This technology is critical for high-resolution subsurface imaging, particularly in complex offshore environments and mature deepwater fields where enhancing recovery and improving drilling accuracy are paramount. Operators are increasingly focused on extracting maximum value from their established fields, a move that aligns with capital discipline and risk mitigation.

This long-term commitment gains particular significance when viewed against recent crude price movements. As of today, Brent Crude trades at $99.13, reflecting a modest daily dip of 0.22%. However, our proprietary 14-day Brent trend data reveals a more telling story: Brent has fallen from $109.27 on April 7th to $99.78 on April 24th, representing a substantial decline of approximately 8.7% over just two weeks. Similarly, WTI Crude currently stands at $94.4, down 1.51% today. This short-term volatility might typically prompt a pause in long-term spending, yet the TGS extension signals a counter-cyclical, strategic investment. It suggests that while energy markets experience daily and weekly swings, major producers are committed to optimizing their high-value deepwater portfolios, indicating a belief in the sustained economic viability of these assets over a multi-year horizon.

Strategic Imperatives: Maximizing Recovery and Capital Efficiency

The essence of the TGS contract extension lies in its focus on optimizing existing fields rather than purely on new exploration. This aligns perfectly with the evolving priorities of major energy producers: improving capital efficiency and maximizing recovery from known reserves. OBN seismic technology provides the detailed subsurface data necessary for precise reservoir characterization, which directly translates into more accurate drilling plans and enhanced production performance. In mature basins like the US Gulf, where infrastructure is established but geological complexities abound, such advanced imaging is crucial for identifying bypassed pay zones, optimizing well placement, and extending the economic life of fields.

TGS CEO Kristian Johansen’s remarks about adapting to “evolving industry priorities” resonate deeply with this theme. It’s not just about finding more oil; it’s about making every barrel count. This pragmatic approach to offshore development reflects a broader industry trend where companies are under pressure to deliver consistent returns and demonstrate responsible resource management. By investing in technology that enhances the productivity of existing assets, operators mitigate the higher risks associated with frontier exploration while ensuring a steady, efficient supply of hydrocarbons. This strategy is particularly compelling in deepwater, where the upfront capital expenditure is substantial, making long-term operational efficiency a critical determinant of project profitability.

Investor Sentiment and the Long-Term Oil Demand Outlook

Our proprietary reader intent data reveals a consistent theme among investors: significant questions about the long-term trajectory of oil demand and crude prices. Queries such as “What would push Brent below $80? What would push it above $120?” and “What’s the impact of EV adoption on long-term oil demand projections?” highlight the underlying uncertainty faced by the market. The TGS contract extension offers a tangible, real-world counterpoint to the more pessimistic narratives surrounding peak oil demand and the rapid decline of conventional hydrocarbon production.

A three-year commitment to deeply invest in the production efficiency of existing deepwater assets suggests that major operators continue to foresee robust demand for conventional oil for the foreseeable future, certainly beyond 2029. This isn’t a speculative bet on new discoveries; it’s an investment in the long-term productivity of established assets. It signals that while the energy transition is undeniably underway, the pace of decline for high-quality, lower-carbon-intensity barrels from optimized deepwater fields is not as rapid as some models project. Companies are making multi-year capital allocation decisions based on a pragmatic assessment of global energy needs, underscoring their belief that conventional oil will remain a vital component of the energy mix for decades, making these efficiency-driven investments entirely rational and necessary for sustained profitability.

Upcoming Events: Gauging Broader Industry Trajectories

While the TGS extension provides a specific view into deepwater investment, broader industry trends will be further illuminated by upcoming market events. Investors should closely monitor key releases that offer insights into supply, demand, and overall activity levels, which can either reinforce or challenge the long-term investment rationale demonstrated by this contract.

The Baker Hughes Rig Count, scheduled for May 1st and May 8th, will be a critical indicator of overall drilling activity across North America, including offshore. A sustained or increasing rig count would further validate the need for services like those provided by TGS, suggesting continued investment in both development and exploration. Furthermore, the EIA Short-Term Energy Outlook, due on May 2nd, will provide updated forecasts for global oil supply and demand. This comprehensive report will be instrumental in shaping long-term market sentiment, offering valuable context on whether current investments in production optimization align with projected energy requirements. Weekly inventory reports from the API (April 28th, May 5th) and EIA (April 29th, May 6th) will offer immediate snapshots of market balances, but it is the forward-looking outlooks and sustained activity indicators that will truly gauge the industry’s trajectory and the continued appetite for deepwater capital allocation.

The TGS contract extension is a clear indicator that despite short-term price volatility and long-term energy transition discussions, optimizing existing deepwater assets remains a high priority for major operators. This strategic investment in efficiency and recovery highlights a pragmatic approach to ensuring sustained profitability and demonstrates confidence in the enduring role of conventional oil in the global energy landscape for years to come. Savvy investors will recognize this as a signal of fundamental strength and strategic foresight in a dynamic market.