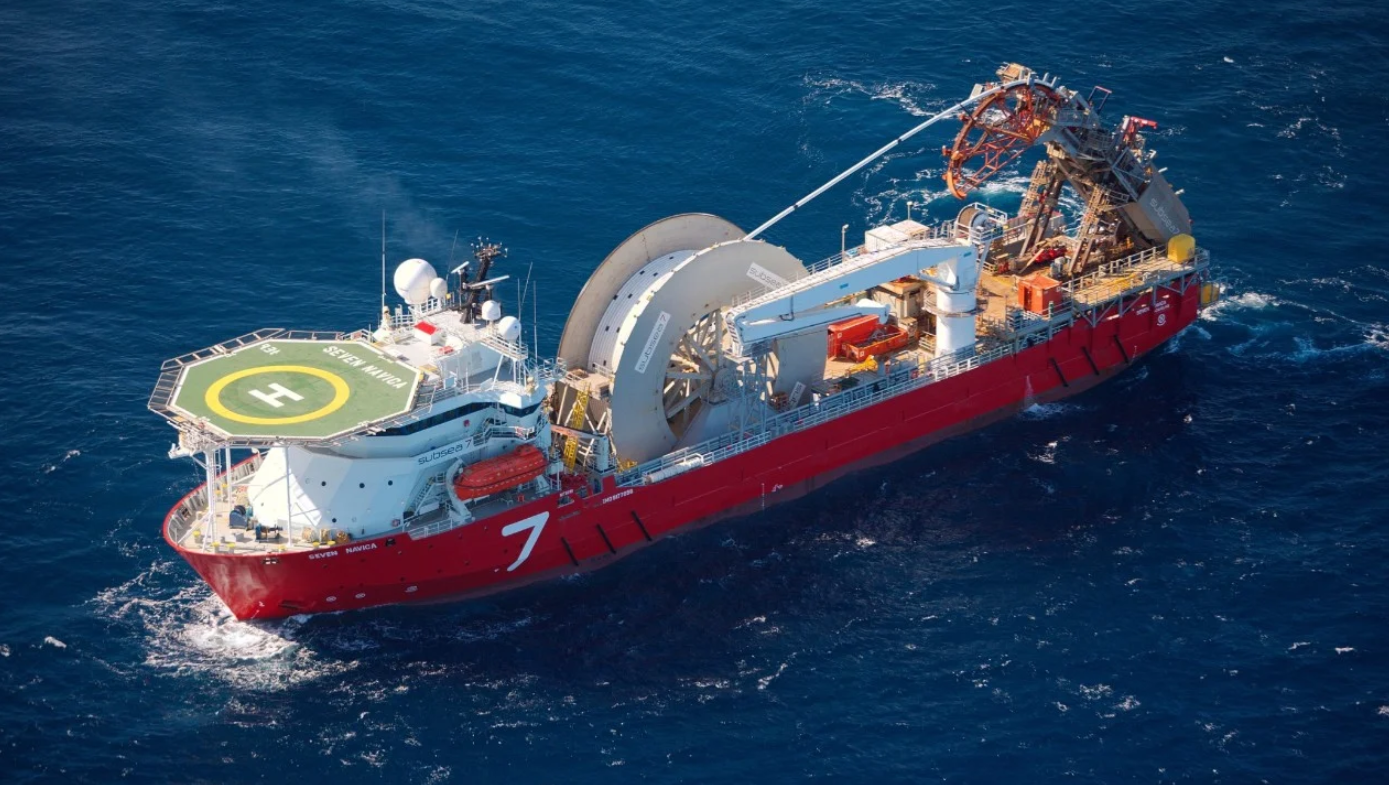

The global energy sector continues to demonstrate robust activity, particularly within the crucial offshore segment. Today’s news of Subsea7 securing a substantial contract in West Africa underscores a renewed confidence in deepwater developments, signaling positive momentum for the oil and gas services industry. This award, categorized as “sizeable” by Subsea7, meaning a value between $50 million and $150 million, involves the intricate work of transporting and installing flexible pipelines, umbilicals, and associated subsea components essential for connecting a floating production, storage and offloading (FPSO) vessel. Additionally, it encompasses pre-laying activities for a future drilling campaign, with project management commencing immediately in the UK and France, and critical offshore operations slated for 2026. This development provides a timely lens through which to examine the health of the offshore market, its drivers, and what investors should anticipate in the near term.

West Africa’s Enduring Appeal and Subsea7’s Strategic Foothold

West Africa has long been a cornerstone of global offshore oil production, characterized by significant deepwater reserves and a consistent drive for new discoveries and infrastructure upgrades. This latest contract solidifies Subsea7’s strategic presence in the region, a critical area for major energy companies seeking to bolster long-term production. The scope of work, specifically the integration with an FPSO and preparatory work for future drilling, highlights the comprehensive capabilities required for modern offshore projects. For investors, this contract award represents more than just a revenue stream for Subsea7; it’s an indicator of sustained capital expenditure in a high-value basin. The immediate start of engineering and project management, despite offshore activity not commencing until 2026, speaks to the long lead times inherent in complex subsea developments. This forward visibility in order books is a key metric analysts monitor for offshore service providers, offering a degree of revenue predictability in an otherwise volatile market. Subsea7’s ability to secure such a foundational contract demonstrates not only its technical prowess but also its strong client relationships in a competitive landscape.

Offshore Investment Momentum Amidst Favorable Market Dynamics

The decision to sanction and award significant offshore contracts like this one is intrinsically linked to the prevailing oil price environment and the long-term outlook for energy demand. As of today, Brent Crude trades at $96.04 per barrel, reflecting a 1.32% gain for the day, with its range settling between $91 and $96.26. WTI Crude also shows strength at $92.4, up 1.23%. While Brent has experienced some volatility, trending down from $102.22 on March 25th to $93.22 on April 14th – a nearly 8.8% decline over two weeks – the current price point remains robust and highly supportive of deepwater exploration and production. Such price levels offer attractive returns for capital-intensive projects, providing the necessary incentive for operators to invest in new production capacity. Investors are keenly observing these price movements, and a key question emerging from our proprietary reader intent data this week revolves around building a base-case Brent price forecast for the next quarter, alongside a consensus 2026 Brent forecast. This contract, with its 2026 offshore start date, suggests that the underlying operator is confident in sustained favorable oil prices well into the middle of the decade, aligning with the broader industry’s growing consensus around a higher-for-longer price environment that underpins long-cycle investments.

Upcoming Catalysts and Investor Outlook for Deepwater

The timing of this contract award also coincides with a period of significant market-moving events that will further shape the investment landscape for offshore energy. In the coming days, investors will be closely monitoring the Baker Hughes Rig Count on April 17th and April 24th, offering insights into drilling activity trends. More critically, the OPEC+ Joint Ministerial Monitoring Committee (JMMC) meeting on April 18th, followed by the Full Ministerial OPEC+ Meeting on April 20th, will be pivotal. Any decisions regarding production quotas could significantly influence crude prices and, consequently, the appetite for future offshore developments. Additionally, the API Weekly Crude Inventory (April 21st, April 28th) and EIA Weekly Petroleum Status Report (April 22nd, April 29th) will provide fresh data on supply-demand balances. These events are crucial for investors seeking to refine their oil price forecasts and understand the macro environment driving contracting activity in the subsea sector. Given that offshore projects are multi-year endeavors, the long-term strategic decisions by OPEC+ and the ongoing inventory trends provide critical context for assessing the risk-reward profile of companies like Subsea7. The sustained interest in deepwater, evidenced by this contract, suggests a belief that global demand will continue to require these complex, high-yield assets, irrespective of shorter-term market fluctuations.

Broader Implications for the Offshore Services Ecosystem

Subsea7’s West Africa contract is not an isolated event; it’s a significant bellwether for the broader offshore services ecosystem. The transport and installation of flexible pipelines, umbilicals, and associated subsea components are highly specialized tasks, requiring a sophisticated supply chain. This award implies a ripple effect, potentially boosting demand for sub-suppliers of materials, specialized vessels, and skilled labor. As the industry emerges from a period of underinvestment, particularly in deepwater, such contracts indicate a healthy resurgence in capital allocation towards complex, long-cycle projects. This trend bodes well not only for direct competitors but also for ancillary service providers in areas like engineering, procurement, construction, and installation (EPCI). The commitment to offshore activity in 2026 suggests that oil and gas companies are now making investment decisions with a multi-year horizon, prioritizing energy security and reliable supply amidst evolving geopolitical and energy transition narratives. For investors, this signals a potential re-rating for companies with strong offshore exposure and robust backlogs, as the cycle for deepwater investment appears to be gaining sustainable momentum.