Calgary, Alberta – In a definitive move reshaping its operational landscape, Strathcona Resources Ltd. (TSX: SCR), a prominent player in the Canadian energy sector, has announced the successful negotiation of agreements to divest a substantial portion of its Montney assets. These three separate transactions collectively command an impressive valuation of approximately $2.84 billion, signaling a significant strategic pivot for the company as it reorients towards becoming a pure-play heavy oil producer. This major financial maneuver is set to unlock considerable value and sharpen Strathcona’s operational focus, presenting a clear trajectory for investors in the evolving upstream oil and gas market.

Major Asset Sales Redefine Strathcona’s Portfolio

The comprehensive divestment strategy encompasses three distinct asset sales, each contributing significantly to the total consideration. These transactions underscore the robust demand for high-quality Montney resource plays within the Canadian energy landscape, attracting key industry players:

- Kakwa Asset Sale to ARC Resources Ltd.: Strathcona will transfer its Kakwa asset to ARC Resources Ltd. for an approximate total value of $1,695 million. This comprises $1,650 million in cash, alongside the assumption of approximately $45 million in lease obligations by ARC. This transaction is anticipated to close early in the third quarter of 2025, pending regulatory approvals and standard closing conditions.

- Grande Prairie Asset Divestment: A separate agreement covers the sale of Strathcona’s Grande Prairie asset, valued at approximately $850 million. This deal includes $750 million in cash and the purchaser assuming approximately $100 million in lease obligations. This sale is also slated for an early third-quarter 2025 completion, subject to similar regulatory and customary closing conditions.

- Groundbirch Asset Sale to Tourmaline Oil Corp.: The Groundbirch asset will change hands to Tourmaline Oil Corp. in exchange for $291.5 million in common shares of Tourmaline. This share-based consideration provides Strathcona with a strategic equity stake in another leading Canadian producer. The Groundbirch sale is expected to finalize in the second quarter of 2025, contingent on regulatory approvals. Notably, the share consideration is not subject to any lock-up periods beyond the standard four-month statutory hold, though Strathcona has expressed no immediate plans to dispose of these shares, indicating confidence in Tourmaline’s future performance.

Financial Performance and Valuation Insights

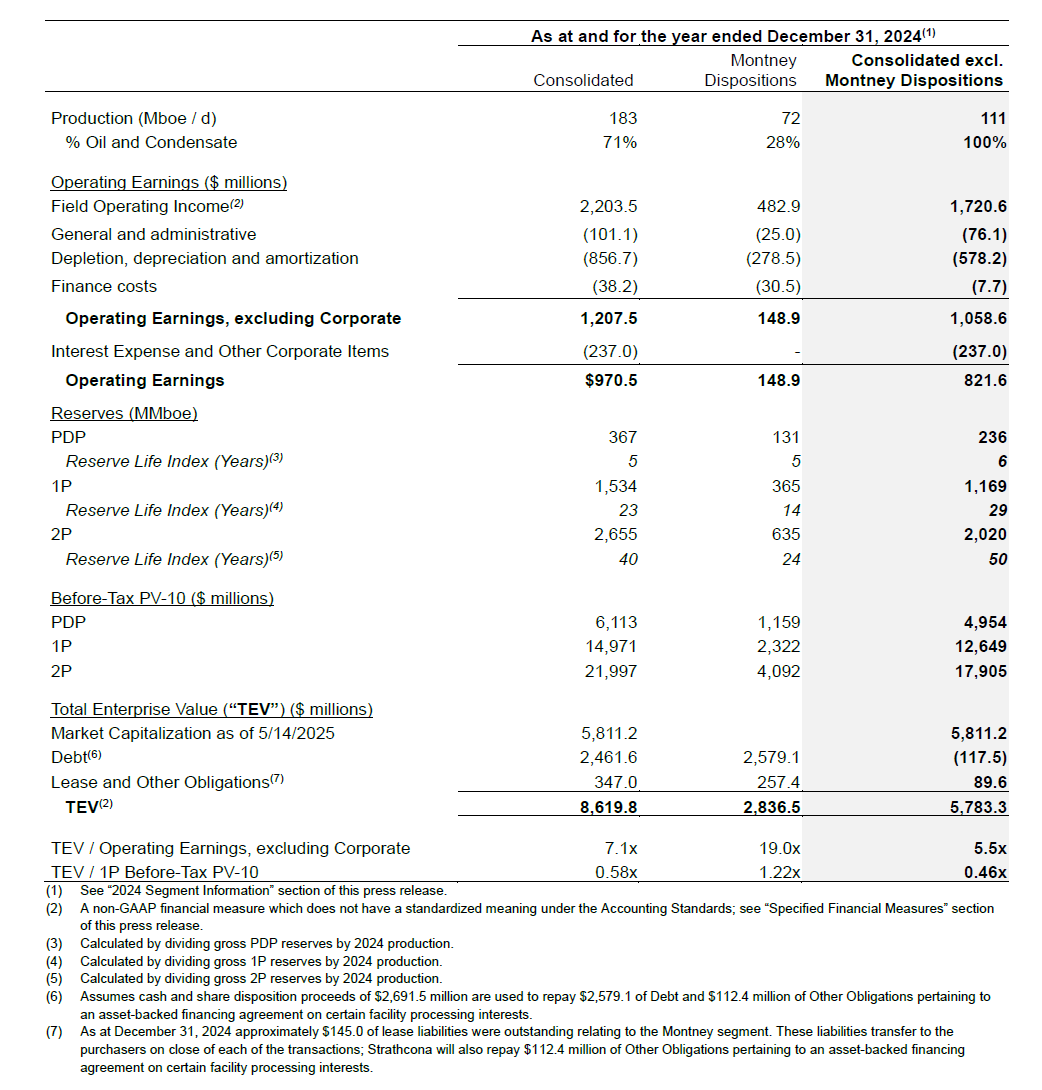

Examining the financial implications, the divested Montney assets, while significant, represented a concentrated portion of Strathcona’s overall financial output in 2024. These assets collectively generated $149 million in operating earnings for the year ended December 31, 2024, which constituted 12% of Strathcona’s total operating earnings, excluding interest and other corporate items. From a valuation perspective, their year-end 2024 proved PV-10 before-tax stood at approximately $2.3 billion, accounting for 15% of the company’s total proved PV-10 for the same period. The combined sale price of approximately $2.84 billion represents a substantial 33% of Strathcona’s current enterprise value, highlighting the magnitude of this strategic repositioning and the premium achieved for these non-core assets.

For investors, this valuation provides a compelling snapshot of management’s ability to monetize assets effectively. The cash proceeds, totaling $2.4 billion from the Kakwa and Grande Prairie sales alone, will significantly bolster Strathcona’s balance sheet, offering substantial financial flexibility. This capital can be strategically deployed for debt reduction, investment in its core heavy oil operations, or potential capital returns to shareholders, all of which are critical considerations for upstream oil and gas investment decisions.

Strategic Rationale: A Clear Path to Heavy Oil Specialization

The overarching strategic objective behind these divestments is to transform Strathcona into a pure-play heavy oil company. This specialization allows for a more streamlined operational focus, potentially enhancing efficiency and optimizing capital allocation within a specific segment of the energy market. By shedding its Montney dry gas and liquids-rich assets, Strathcona is concentrating its efforts on its established heavy oil production base, where it believes it can generate superior returns and achieve a competitive advantage. This strategic clarity is often favored by investors seeking focused exposure within the diverse energy sector.

Furthermore, the transaction is highly tax-efficient for Strathcona. The company reported $5.5 billion in tax pools as of March 31, 2025, and does not anticipate incurring any cash taxes as a result of these Montney dispositions. This allows the full value of the sale proceeds to be utilized for corporate objectives without immediate erosion from tax liabilities, a significant advantage in large-scale asset transactions.

Operational Excellence and Synergistic Opportunities for Buyers

The journey of Strathcona’s Montney assets is a testament to the team’s operational prowess. Under the leadership of President Al Grabas, the Montney business experienced remarkable growth, expanding from a modest 5 Mboe/d in January 2017 to an impressive 72 Mboe/d by 2024. This trajectory underscores the quality and productive potential of the assets now changing hands.

The acquiring companies, ARC Resources and Tourmaline Oil Corp., are both well-established and highly regarded operators in the Canadian energy sector. Strathcona has acknowledged the “hand-in-glove fit” of these assets with the purchasers’ existing operations. Both ARC and Tourmaline possess extensive track records of first-class operations in the surrounding areas, suggesting that these assets will seamlessly integrate into their portfolios. This synergy is expected to enable the new owners to maximize value from the acquired properties, benefiting from economies of scale, shared infrastructure, and optimized operational strategies.

Investor Outlook: A Leaner, More Focused Strathcona

Upon the successful completion of these Montney dispositions, Strathcona Resources will emerge as a leaner, more focused entity dedicated exclusively to heavy oil production. While specific updated guidance on post-disposition production volumes and a long-range plan are still forthcoming, the strategic direction is unequivocally clear. Investors can anticipate a company with a strengthened balance sheet, reduced complexity, and a concentrated effort on maximizing value from its heavy oil assets.

The substantial cash proceeds from these sales provide Strathcona with significant optionality. This capital infusion creates opportunities for accelerated debt reduction, which can lower financial risk and improve credit metrics. Alternatively, it could fund organic growth initiatives within its heavy oil portfolio or pave the way for potential share buybacks or dividend enhancements, directly benefiting shareholders. The strategic investment in Tourmaline shares also positions Strathcona to benefit from the ongoing success of a major natural gas producer, offering a diversified, albeit indirect, exposure to the broader energy market. For those interested in focused heavy oil exposure with a robust financial foundation, Strathcona’s recent moves mark a pivotal and compelling development in the Canadian upstream sector.