Russia’s Oil Sector Defies Expectations with Record Drilling Surge

Russia’s oil producers are executing an extraordinary surge in drilling operations, reaching levels not witnessed in at least five years. This significant uptick in activity, now more than one-third above pre-war benchmarks, signals a robust strategic posture for the nation’s energy sector. For savvy investors tracking global oil and gas dynamics, this sustained performance underscores the Russian oil industry’s remarkable adaptability and its enduring influence on the global energy landscape, even amidst ongoing geopolitical pressures and potential shifts in OPEC+ production quotas.

The accelerated drilling pace serves as a compelling indicator of the industry’s success in navigating Western sanctions. These restrictions were explicitly designed to impair Russia’s long-term capacity for crude extraction by limiting access to advanced technologies and essential equipment. Yet, the sector appears to be thriving, maintaining a formidable output capability that starkly challenges earlier predictions of its decline and offers a critical perspective for energy market participants.

Sustained Production Capacity Amidst Geopolitical Headwinds

Despite the comprehensive nature of the sanctions regime, Russia’s total operational capacity for producing crude oil and condensate remains remarkably robust. Industry experts estimate this capacity stands firmly between 11 million and 11.5 million barrels per day. Significantly, this figure has remained virtually unchanged since 2016, highlighting the unexpected effectiveness of domestic adaptation strategies and the successful establishment of alternative supply chains. This stability in potential output capacity is a key data point for any investor assessing long-term global oil supply and demand.

Ronald Smith, a recognized authority at Emerging Markets Oil & Gas Consulting Partners LLC, confirms that the Russian oilfield service industry has largely “successfully adapted” to the sanctions environment. While acknowledging that perfect, like-for-like replacements might not exist in every instance, Smith emphasizes that “suitable substitutes” have been widely integrated across operations. This strategic pivot ensures the ongoing viability of exploration and production activities, offering a crucial perspective for investors evaluating global oil supply dynamics and the long-term outlook for Russian energy assets in a complex market.

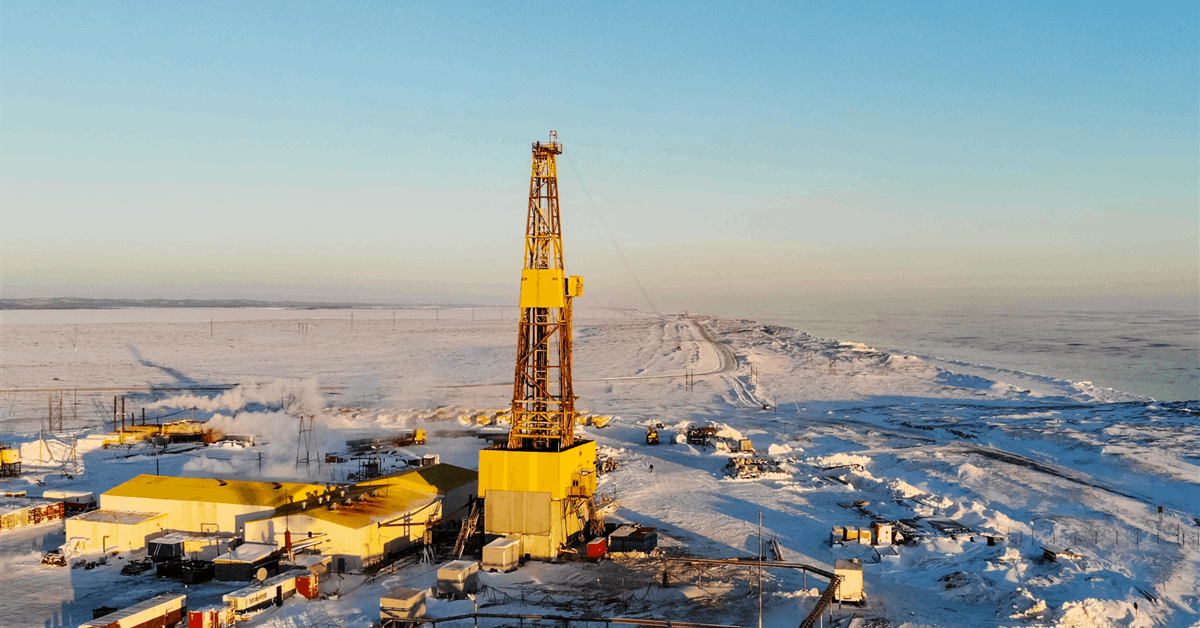

Unprecedented Drilling Activity Fuels Future Output

Tangible evidence of this profound adaptation is clearly reflected in recent drilling metrics. Data reveals that Russia’s production drilling averaged more than 2,370 kilometers, or approximately 7.8 million feet, during January and February of this year. This robust figure surpasses the seasonal averages recorded even in the initial three years following the 2022 invasion, a period that triggered extensive restrictions on Western oilfield services in the region. Such sustained, high-intensity drilling is absolutely crucial for offsetting natural field depletion and maintaining future output levels, signaling confidence in the nation’s ability to extract oil efficiently for years to come.

The mechanisms underpinning this resilience are multifaceted and represent a significant strategic overhaul. While many major foreign service providers exited the Russian market post-invasion, several strategically sold their local units to Russian managers. This clever maneuver ensured that critical equipment and specialized expertise remained available within the country, preventing a complete collapse of vital services. For instance, companies like Schlumberger sold their Russian arm, which was subsequently renamed, and Weatherford International also divested its local operations, ensuring continuity for field operations.

Strategic Adaptations and New Supply Chains Power Resilience

Beyond simply acquiring divested foreign assets, Russian companies have actively expanded their own in-house service divisions. Notably, Gazprom Neft has aggressively grown its specialized oilfield service operations, reducing reliance on external providers. This strategic shift towards self-sufficiency is complemented by significant investment in domestic equipment manufacturing. Russian firms are rapidly developing and producing their own drilling rigs, pumps, and other essential components, bolstering national industrial capacity and insulating the sector from future external supply shocks.

Furthermore, international partnerships have played a pivotal role in bridging technology gaps. China, in particular, has emerged as a key supplier of drilling rigs, components, and other critical equipment, fostering a new network of trade relationships that circumvents traditional Western supply lines. This diversified sourcing strategy has been instrumental in allowing Russia’s oil and gas sector to maintain, and even increase, its operational tempo, demonstrating a formidable capacity to adapt to a highly challenging global environment.

Surging Domestic Demand and Economic Growth Underpin Stability

The stability of Russia’s oil production is not solely reliant on export markets; robust domestic demand for oil products also plays a significant role. Ministry of Energy data indicates that domestic gasoline consumption rose by 8% in 2023, while diesel consumption increased by 5%. This strong internal demand provides a stable base for crude processing and refined product sales, acting as a buffer against fluctuations in international markets.

This internal strength is mirrored by broader economic resilience. Despite sweeping international sanctions, the International Monetary Fund (IMF) projects Russia’s economy to grow by 2.6% in 2024. This growth is fueled by increased military spending, which stimulates industrial production, and a resilient consumer demand base. Oil and gas revenues remain vitally important for the state budget, underscoring the government’s vested interest in maintaining and expanding hydrocarbon output capabilities. For investors, understanding this dual demand — domestic and international — is crucial for forecasting the sector’s financial health.

Navigating Price Caps and Global Market Dynamics

The market for Russian crude has continued to evolve under the shadow of international price caps. While Brent crude currently trades around $85 a barrel, Russia’s flagship Urals crude typically trades at a discount, recently hovering around $70 a barrel. This represents a discount of approximately $15 a barrel relative to Brent, a figure that has fluctuated since the imposition of sanctions. Despite the Western-imposed price cap of $60 a barrel for Russian oil, Urals crude consistently trades above this threshold, indicating continued market access and strong demand for Russian crude, particularly from non-Western buyers.

This dynamic illustrates the limitations of the price cap mechanism and highlights the enduring market appetite for Russian energy. Investors must recognize that while discounts exist, Russia continues to find buyers for its crude at prices well above the punitive caps, ensuring substantial revenue streams for its energy companies and the national budget. This resilience in market access, coupled with the impressive operational adaptability, positions Russia as an undeniable force in global oil supply for the foreseeable future.

Investment Outlook: A Resilient Force in Global Energy

In conclusion, the Russian oil industry presents a compelling case study in resilience and adaptation. The record drilling surge, sustained production capacity, and strategic pivots toward domestic solutions and new international partnerships underscore a sector that has not only defied expectations but is actively strengthening its long-term operational capabilities. For investors in oil and gas, understanding these profound shifts is paramount.

Russia’s ability to maintain and even increase drilling activity, develop indigenous service capabilities, and secure alternative supply chains suggests a sustained output level that will continue to significantly influence global oil markets and OPEC+ strategy. The enduring strength of its energy sector, backed by robust domestic demand and an adaptive economic framework, solidifies Russia’s position as a critical, albeit complex, player in the international energy arena, demanding careful consideration from any serious market participant.