A recent development from the Austrian firm Resch presents a significant leap in battery technology, potentially slashing production costs by one-third. This innovation, centered on a novel modular design that eliminates adhesives and welds, promises to make electric batteries more affordable, easier to maintain, and simpler to recycle. For oil and gas investors, this isn’t just a technical curiosity; it represents a tangible acceleration of the energy transition, posing a long-term challenge to hydrocarbon demand across multiple sectors. Understanding the implications of such breakthroughs is crucial for navigating the evolving energy landscape and safeguarding investment portfolios.

The Battery Breakthrough and its Economic Implications

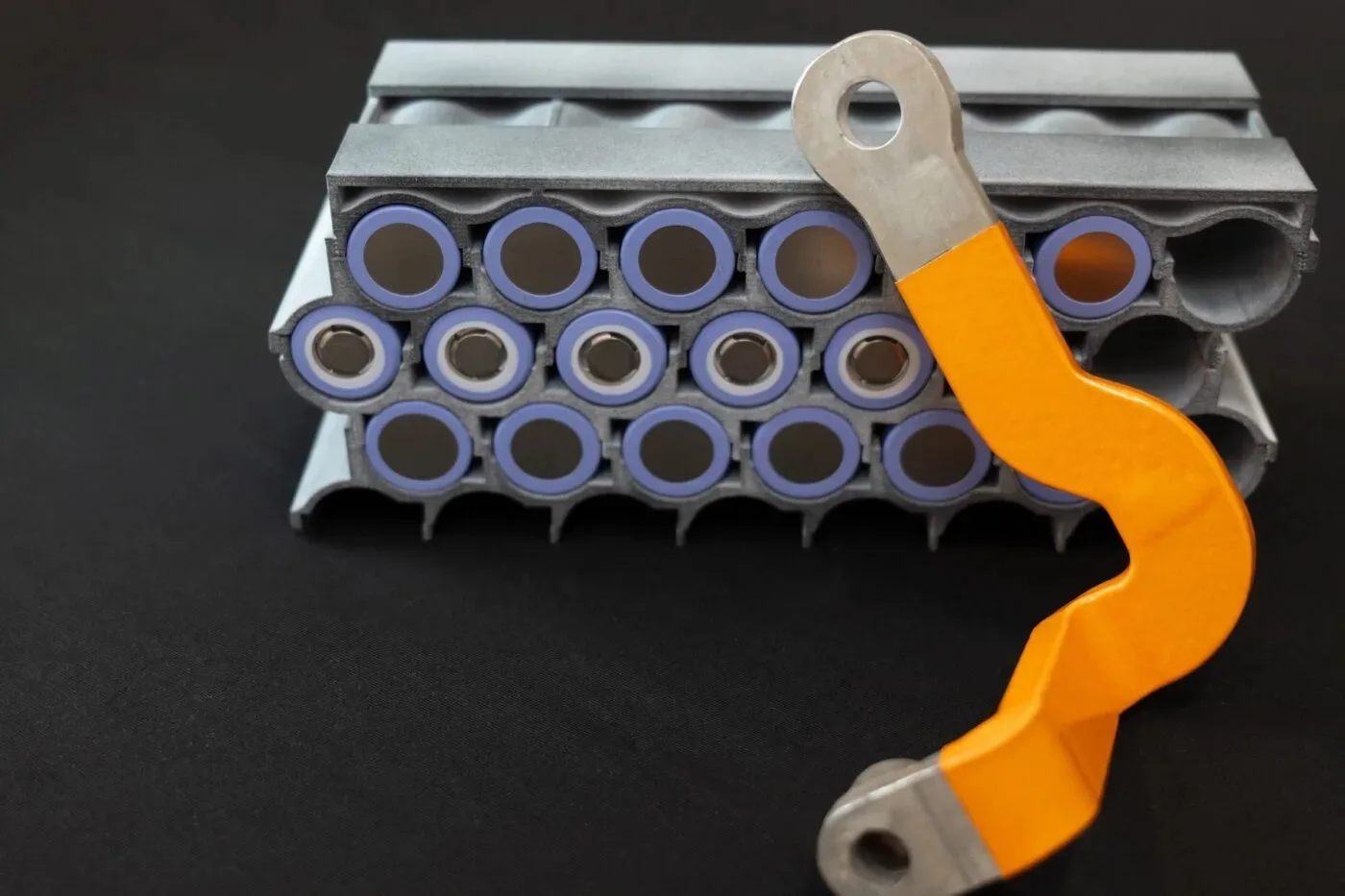

Resch’s new battery module marks a departure from conventional manufacturing, which typically relies on adhesive bonding and welding, especially prevalent among Asian manufacturers. This standard approach, while efficient for production, makes individual cell replacement nearly impossible and complicates end-of-life recycling. Resch’s “revolutionary concept” addresses this by mechanically assembling cells, allowing for targeted replacement of defective units – akin to building with Lego. This design not only enhances reparability but also simplifies the recycling process at the battery’s end of life. Crucially, the module is compatible with all standard cell formats, offering broad applicability.

The most compelling aspect for market participants is the projected cost reduction. Resch anticipates a cost saving of up to one-third if their solution enters series production. Such a significant reduction directly impacts the total cost of ownership for electric vehicles (EVs), electric aircraft, ships, and stationary battery storage systems. Lower battery costs make these electric alternatives more competitive against their fossil fuel-powered counterparts, accelerating adoption rates and, consequently, diminishing future demand for oil and gas products. The implications extend beyond automotive, hinting at a broader electrification wave impacting heavy-duty transport and grid stability, areas traditionally reliant on hydrocarbons.

Market Realities and the Immediate Horizon for Oil Investors

While long-term trends like battery cost reductions are critical, oil and gas investors must also contend with immediate market dynamics. As of today, Brent crude trades at $90.38, reflecting a notable 9.07% drop within the day’s range of $86.08 to $98.97. WTI crude similarly saw a significant decline of 9.41% to $82.59, while gasoline prices are down 5.18% to $2.93. This daily volatility follows a broader trend, with Brent having fallen by 18.5% — a substantial $20.91 — from $112.78 on March 30th to $91.87 just yesterday.

These fluctuations underscore that despite the march of electrification, current oil prices are still heavily influenced by supply-demand imbalances, geopolitical tensions, and macroeconomic indicators. The immediate impact of a battery innovation, even one as promising as Resch’s, is dwarfed by these daily and weekly market forces. Oil and gas investors are currently navigating a complex environment where short-term trading opportunities and hedging strategies remain paramount, even as the long-term narrative of demand destruction gains momentum.

Catalysts and Constraints: The Path to Market Domination

The transition from a promising prototype to widespread market adoption for Resch’s battery technology is not instantaneous. Several automotive OEMs are currently evaluating the solution for series production, and the design is explicitly engineered for fully automated manufacturing, indicating a pathway to high-volume output. The stated goal of launching a “market-ready solution from Europe” also points to strategic positioning within the global supply chain.

However, the pace of adoption will be critical. In the short term, global energy markets will be heavily influenced by traditional supply-side dynamics. Investors will keenly watch the upcoming OPEC+ Joint Ministerial Monitoring Committee (JMMC) meeting tomorrow, April 18th, followed by the full Ministerial meeting on April 19th. Any shifts in production quotas from these gatherings could trigger significant price movements, momentarily overshadowing technological advancements. Further weekly insights will come from the API and EIA crude inventory reports on April 21st and 22nd, and again on April 28th and 29th, alongside the Baker Hughes Rig Count on April 24th and May 1st. These events will dictate near-term market sentiment, but the ongoing development of cost-effective, modular battery solutions like Resch’s continues to lay the groundwork for a future where oil demand growth is increasingly constrained.

Investor Sentiment and the Long-Term Outlook for Hydrocarbons

Our proprietary reader intent data shows investors are intensely focused on forecasting oil prices, with common queries like “what do you predict the price of oil per barrel will be by end of 2026?” and “How well do you think Repsol will end in April 2026” dominating discussions. This reflects a clear anxiety about future demand and commodity price stability, exacerbated by technological advancements in renewables and energy storage.

The potential for a 33% reduction in battery costs, as proposed by Resch, directly impacts this long-term outlook. It signifies a significant step towards achieving cost parity, or even superiority, for electric powertrains and energy storage solutions. For investors in exploration and production (E&P) companies, refining, and integrated majors, this trend necessitates a re-evaluation of long-term asset values and investment strategies. While oil and gas will undoubtedly remain crucial for petrochemicals and certain hard-to-abate sectors for decades, the growth trajectory, particularly in transport fuels, is under existential threat. Companies with robust diversification strategies, investments in carbon capture, or strong positions in future fuels will likely be better positioned to weather this transition. Investors must scrutinize the resilience of their oil and gas holdings against accelerating electrification, driven by innovations that make alternatives increasingly attractive.