The Philippines is aggressively charting a course toward a renewable energy-dominated future, a strategic shift that carries significant implications for global fossil fuel demand, particularly within the dynamic Southeast Asian market. The Department of Energy (DOE) has unveiled an ambitious pipeline of Green Energy Auction Program (GEAP) rounds, targeting substantial renewable capacity additions over the next decade. This programmatic clarity, designed to attract developers and capital, signals a structural shift in the nation’s energy mix, challenging the long-term outlook for traditional oil and gas investments in the region. For investors, understanding the velocity and specifics of this transition is paramount, especially when navigating the inherent volatility of today’s crude markets.

Philippines’ Renewable Energy Blueprint: A Decade of Disruption

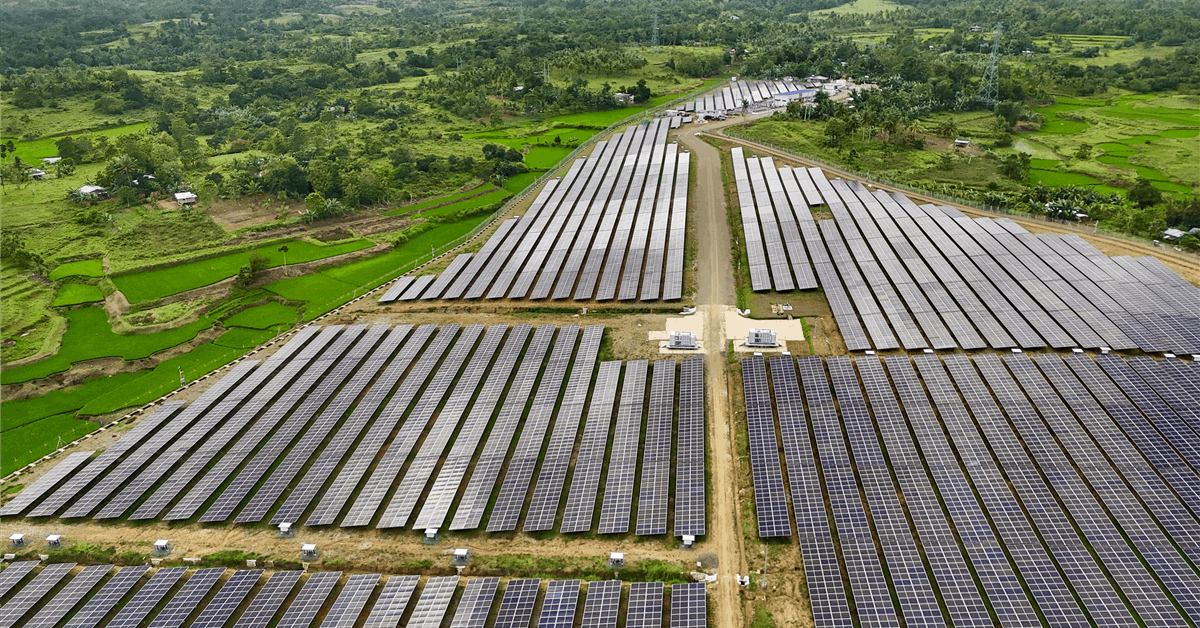

The Philippine DOE’s latest announcement details the sixth to ninth rounds of its Green Energy Auction Program, spanning project deliveries from 2027 to 2035. This comprehensive plan aims to install an impressive 25 gigawatts (GW) of renewable power capacity by 2035, with specific targets including over 3,200 megawatts (MW) of non-floating solar capacity between 2027 and 2028, and an additional 5,565 MW from diverse technologies such as onshore wind, floating solar, rooftop solar, battery energy storage systems (BESS), agri-solar, canal-top solar, biomass, geothermal, and hydropower, delivered between 2028 and 2035. This structured approach, as emphasized by Energy Secretary Sharon S. Garin, provides crucial market visibility for developers and financial institutions, facilitating capital mobilization and project delivery. With targets of 35 percent renewable energy share by 2030 and 50 percent by 2040, the nation is positioning itself as a leader in the regional energy transition, systematically reducing its reliance on imported fossil fuels for power generation. While the Philippines added over one GW of capacity in 2025, predominantly from renewables, the inclusion of one oil-run and one natural gas-run plant highlights the current transitional phase, which these new auctions aim to accelerate away from.

Market Volatility vs. Long-Term Energy Transition

While the Philippines lays out its long-term renewable energy vision, crude oil markets continue to exhibit significant short-term volatility. As of today, Brent Crude trades at $92.24 per barrel, marking a +2% increase for the day, with WTI Crude at $88.73, up +1.5%. This daily uptick offers a momentary reprieve after a challenging period, as Brent Crude experienced a notable 14-day downturn, shedding nearly 20% from $118.35 on March 31 to $94.86 on April 20. Such sharp swings understandably generate investor anxiety, a sentiment clearly reflected in our proprietary reader intent data, which shows a strong focus on immediate price direction, with many asking whether WTI is poised for gains or losses. Additionally, there’s considerable interest in longer-term price predictions, with investors querying the expected price of oil per barrel by the end of 2026. This juxtaposition of short-term price uncertainty and long-term structural shifts, like the Philippines’ aggressive RE push, underscores the complexity for oil and gas investors. While global demand continues to be influenced by geopolitical events and economic cycles, the persistent build-out of renewable capacity in key growth regions serves as a foundational headwind for fossil fuel consumption, particularly in the power sector.

Upcoming Events and Divergent Investment Signals

The coming weeks present a series of critical events that could sway crude markets, demanding careful attention from investors. Tomorrow, April 21, the OPEC+ JMMC Meeting is scheduled, and any statements or indications regarding production policy could trigger immediate price movements. Following this, the EIA Weekly Petroleum Status Reports on April 22 and April 29, along with the Baker Hughes Rig Count on April 24 and May 1, will offer crucial insights into U.S. supply and demand dynamics. Further out, the EIA Short-Term Energy Outlook on May 2 will provide updated forecasts that could shape near-term market expectations. These events predominantly focus on the supply and demand equilibrium of fossil fuels, creating a distinct investment signal compared to the long-term, policy-driven renewable energy pipeline. For sophisticated investors, the challenge lies in reconciling these short-term, fossil-fuel-centric market catalysts with the persistent, long-term narrative of energy transition unfolding in economies like the Philippines. The aggressive rollout of diverse renewable technologies, including the 3,300 MW offshore wind capacity offered in the GEA-5 auction for delivery between 2028 and 2030, represents a structural shift that will incrementally erode demand for traditional power sources, irrespective of immediate crude inventory levels or rig counts.

Investment Implications: Shifting Capital and Regional Dynamics

The Philippines’ resolute commitment to renewable energy development sends a clear signal to the investment community: capital allocation in the regional energy sector is undergoing a fundamental re-evaluation. For oil and gas companies with exposure to Southeast Asia, particularly those involved in power generation fuels like natural gas and fuel oil, this aggressive RE pipeline implies a cap on future demand growth, if not an eventual decline. While the nation added 160 MW of battery energy storage capacity in Luzon and Visayas islands in 2025, and overall installed more than one GW of capacity with a majority being renewables, the strategic push towards 25 GW by 2035 significantly shortens the runway for fossil fuels as primary power sources. Investors should scrutinize company portfolios for their adaptability to this shift. Opportunities may arise in supporting infrastructure for renewables, such as grid modernization, smart energy solutions, and advanced battery storage, rather than solely in upstream or midstream fossil fuel projects. Furthermore, the DOE’s “Philippine Energy Plan 2023-50” also targets a 10 percent energy savings, adding another layer of demand suppression that could impact long-term energy consumption projections. This dual approach of boosting renewables and enhancing efficiency paints a challenging picture for fossil fuel demand growth in one of Asia’s burgeoning economies, compelling a strategic re-think for traditional energy investors.