U.S. Demand Surge Ignites Global Oil Consumption, But Inventory Builds Persist

The global oil market witnessed a welcome uptick in demand over the past week, largely propelled by a significant resurgence in U.S. consumption. This domestic surge was primarily attributed to robust travel activities surrounding the Memorial Day holiday, traditionally marking the unofficial start of the American summer driving season. However, despite this positive momentum, the broader picture for global demand expansion continues to track below some expert projections, according to analysis from a leading financial institution.

As of May 28, the monthly expansion in worldwide oil demand is charting at approximately 400,000 barrels per day. While this represents an improvement, analysts from J.P. Morgan’s Commodities Research team noted that this expansion remains roughly 250,000 barrels per day below their initial expectations. This discrepancy highlights the ongoing complexities and mixed signals within the energy sector, prompting careful consideration from investors.

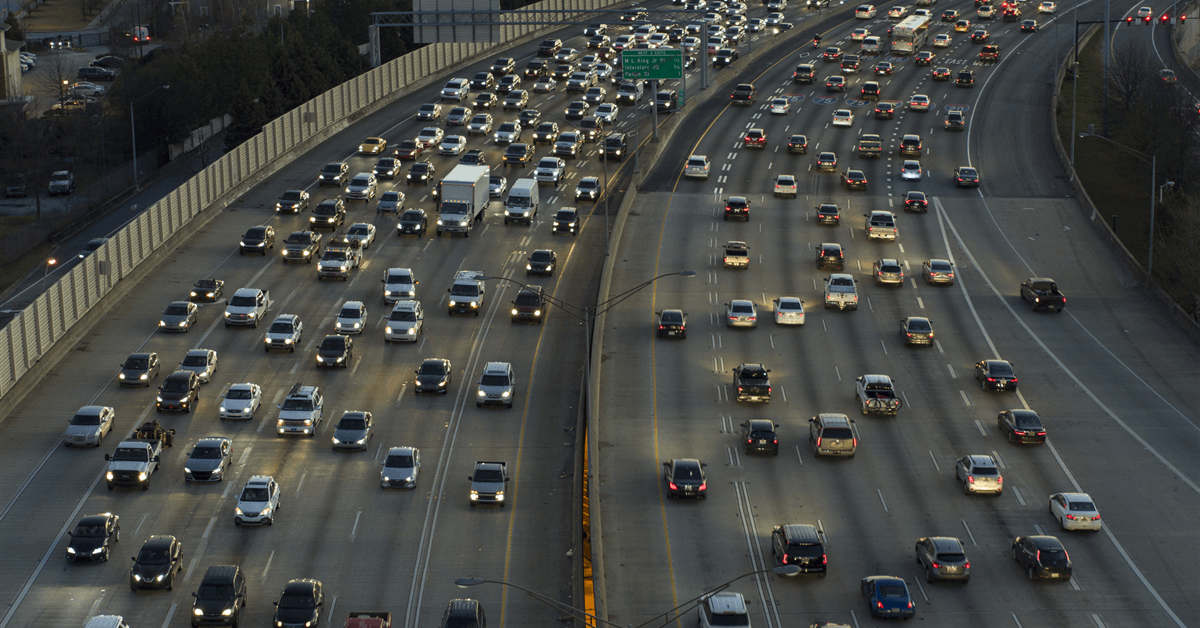

American Consumers Drive Fuel Demand Higher

In line with expectations, global oil demand demonstrated an increase over the preceding week, a direct reflection of heightened U.S. consumer activity. The Memorial Day weekend, a pivotal period for leisure travel, triggered a substantial boost in demand for both gasoline and jet fuel across the nation. This seasonal pattern, coupled with the official commencement of the U.S. summer driving season, typically provides a reliable uplift to fuel consumption.

Beyond personal travel, commercial logistics also signaled stronger energy requirements. U.S. distillate demand experienced a notable surge, mirroring a significant improvement in weekly container arrivals and overall port activity. Data from the Port of Los Angeles, a key indicator of trade flows, showed container arrivals climbing from 75.7 thousand units to an impressive 102.8 thousand units last week. This uptick in freight movement directly translates to increased demand for diesel and other distillate products, underscoring a broader economic pulse.

For American motorists, the price at the pump remained a key consideration. While the average U.S. gasoline price did not decline as sharply as some had predicted for Memorial Day, it nonetheless presented one of the most affordable holiday periods since 2021. Furthermore, when adjusted for inflation, gasoline prices were among the most economical in nearly a decade, a factor that likely encouraged increased road travel and contributed to the observed demand surge.

Inventory Levels Continue to Expand

While demand showed signs of life, the supply side continued to build, impacting inventory levels across key regions. In the fourth week of May, visible commercial oil inventories within the OECD nations—comprising the U.S., Europe, and Singapore—saw an increase of two million barrels. This rise was primarily driven by a four-million-barrel expansion in refined oil product inventories, which effectively offset a two-million-barrel reduction in crude oil stocks. Month-to-date, OECD stocks have now expanded by a significant 30 million barrels, indicating a robust accumulation trend.

On a broader global scale, total liquid inventories also edged upward slightly from the previous week. Crude oil stocks experienced a minor decline of one million barrels, while oil product inventories increased by two million barrels. This delicate balance reflects ongoing production and refining activities against the backdrop of fluctuating consumption. Looking at the month-to-date figures, global liquid inventories have climbed by 63 million barrels, with crude oil stocks contributing a substantial 67 million barrels to this increase, highlighting a persistent build-up in the crude segment.

Recalling Recent Demand Softness

This recent rebound in demand follows a period of notable weakness in the global oil market. In an earlier assessment, J.P. Morgan analysts had reported a softening of global oil demand week-over-week, primarily driven by a decline in U.S. oil consumption. As of May 20, global oil demand had increased by a more modest 340,000 barrels per day, a figure that remained nearly 300,000 barrels per day below the firm’s projections for the month. This prior softness provides crucial context for understanding the current market dynamics and the significance of the Memorial Day boost.

Year-to-date, global oil demand is tracking a growth of 1.0 million barrels per day. While this represents a healthy expansion, it still falls 70,000 barrels per day below J.P. Morgan’s revised growth expectations of 1.1 million barrels per day for the year. This persistent gap between actual demand growth and expert forecasts underscores the cautious approach many analysts are taking when evaluating the overall strength and trajectory of the global oil market.

Investor Outlook: Navigating Mixed Signals

For energy investors, this intricate interplay of fluctuating demand and persistent inventory builds presents a nuanced picture. The strong seasonal surge in U.S. fuel consumption provides a near-term bullish signal, particularly for companies involved in refining and gasoline distribution. However, the broader narrative of global demand expansion falling short of expectations, coupled with rising inventory levels, suggests that underlying market fundamentals may still be facing headwinds. Monitoring these key metrics, particularly the pace of inventory accumulation and the sustained strength of U.S. and international economic activity, will be critical for assessing the future direction of crude oil prices and the overall health of the energy sector.