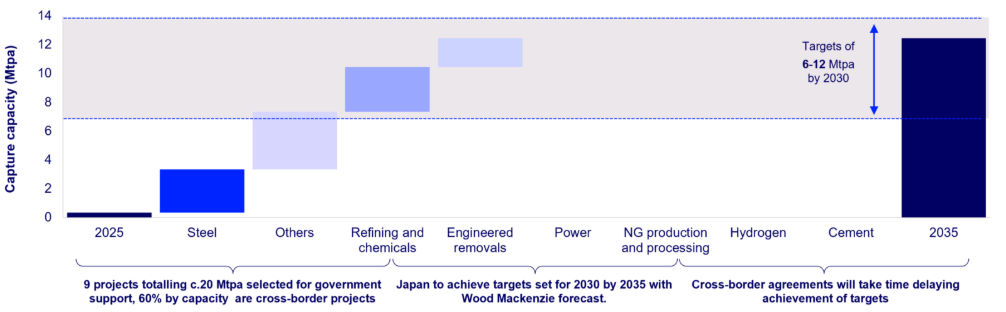

Japan’s carbon capture, utilization, and storage (CCUS) sector stands on the precipice of a monumental expansion, signaling a pivotal shift in the nation’s energy landscape. Our proprietary analysis indicates a projected surge in capacity from current demonstration levels of 0.3 million tonnes per annum (Mtpa) to an ambitious 12.5 Mtpa by 2035. This thirty-fold increase firmly positions Japan as a regional leader in industrial decarbonization, offering compelling long-term investment opportunities for those looking beyond traditional hydrocarbon plays.

Scaling Japan’s Decarbonization Ambition

The sheer scale of Japan’s CCUS commitment underscores its strategic importance. With a target of 12.5 Mtpa by 2035, the country is not merely dabbling in carbon management; it is embedding CCUS as a core pillar of its energy future. This rapid capacity build-up is predominantly driven by hard-to-abate industrial sectors, including steel and petrochemicals, which face significant challenges in reducing emissions through other means. The government has already shortlisted nine advanced carbon capture and storage (CCS) projects, collectively representing over 20 Mtpa of potential capacity. This industrial focus ensures a robust demand base for CCUS services, translating into a tangible market for technology providers, infrastructure developers, and storage operators. For investors, this signals a clear and growing addressable market within a nation committed to achieving its net-zero targets.

The Cross-Border Imperative: Unlocking Storage Potential

While Japan’s capture capacity is set for aggressive growth, a critical bottleneck and corresponding investment opportunity lie in carbon storage. Our data highlights that nearly 60% of the potential 20 Mtpa capacity from advanced projects is reliant on international cross-border storage partnerships. This isn’t just an option; it’s a strategic necessity for Japan to meet its ambitious goals. The challenge, however, comes with cost. Transporting captured emissions internationally, for instance, from Japan to Australia, could escalate costs by 7 to 9 times compared to domestic storage options. Yet, this challenge also presents a unique opportunity for early movers. Strategic partnerships and securing prime storage fields can mitigate overall cost increases to a more manageable 15-20%. The race to establish robust bilateral agreements for cross-border carbon transport will define competitive advantage in the coming decade, making this a crucial area for investors to monitor closely. Success in these negotiations will be instrumental in bridging the gap between Japan’s capture capabilities and its long-term storage needs.

Policy Stability Counteracts Market Volatility for CCUS Investors

Investors frequently ask about the long-term outlook for energy prices, with questions like “what do you predict the price of oil per barrel will be by end of 2026?” dominating our reader intent signals. This reflects a broader concern about market volatility. As of today, Brent crude trades at $89.11, down over 10% from recent highs and a substantial drop from $112.57 recorded just weeks ago. WTI crude mirrors this trend at $81.73, also down significantly. However, for investors eyeing the CCUS sector, Japan offers a contrasting narrative of policy stability and long-term commitment that can insulate against such short-term commodity price swings. Japan now ranks as the second-most CCUS policy-ready nation in Asia Pacific, trailing only Australia, according to our analysis. The country excels in establishing clear, quantifiable CCUS targets and providing access to low-cost funding. Its legislated net-zero targets and robust storage regulatory regime are on par with global leaders. Furthermore, the transition of Japan’s GX ETS from voluntary to mandatory status, coupled with new fuel tax levies, is creating increasingly strong economic incentives for CCUS adoption across industrial sectors. This strong policy framework provides a predictable and supportive environment, offering a more stable investment thesis compared to the fluctuating dynamics of traditional oil markets.

Navigating the Future: Key Events and Long-Term Trajectories

While the immediate energy calendar is punctuated by significant events like the upcoming OPEC+ Joint Ministerial Monitoring Committee (JMMC) meeting on April 17th and the Full Ministerial meeting on April 18th, which will undoubtedly influence short-term crude supply and prices, the trajectory of Japan’s CCUS sector operates on a different, more strategic timeline. Investors should closely watch for developments in bilateral agreements for cross-border carbon transport, as these are critical to realizing the full potential of Japan’s capture ambitions. Our analysis indicates that while Japan is on track to significantly increase its capture capacity, the finalization of these international agreements may push the achievement of its 2030 targets closer to 2035. This emphasizes that while traditional oil market indicators like weekly API and EIA inventory reports (scheduled for April 21st and 22nd, respectively) offer short-term trading signals, the CCUS landscape demands a long-term perspective. Future announcements regarding new project Final Investment Decisions (FIDs) in CCUS infrastructure, particularly those involving international partners, will be key indicators of progress. For the astute investor, understanding this longer-term arc, distinct from the daily commodity price movements, is essential for capitalizing on Japan’s decarbonization journey.