The Accelerating Shift: Leipzig’s E-Bus Order and its Ripple Effect on Oil Demand

While a single order for electric buses in Germany might seem like a mere blip on the radar of global energy markets, the recent decision by Regionalbus Leipzig to acquire nine eCitaro electric buses from Daimler Buses, with an option for 18 more, serves as a potent microcosm of the accelerating energy transition. This isn’t just about replacing a few diesel vehicles; it’s a strategic move towards a fully battery-electric fleet by the early 2040s, complete with dedicated charging infrastructure. For oil and gas investors, such commitments from public transport operators, when aggregated globally, represent a tangible and growing threat to long-term demand fundamentals, especially for refined products like diesel. Understanding these localized yet globally significant shifts is crucial for navigating an increasingly complex investment landscape, particularly as market volatility continues to define commodity prices.

The Persistent Drumbeat of Demand Destruction in Public Transport

The electrification initiative undertaken by Regionalbus Leipzig, transitioning its 160-vehicle fleet from predominantly diesel to battery-electric, exemplifies a trend that is steadily eroding fossil fuel demand in the transportation sector. While the initial nine buses by early 2027 and potential 18 by mid-2028 may seem modest, the long-term goal of full fleet conversion by the early 2040s is a clear signal of intent. This move aligns with broader municipal and national sustainability targets across Europe, where public transport operators are increasingly mandated or incentivized to decarbonize. For oil markets, this translates into a gradual but irreversible decline in diesel consumption. As of today, Brent Crude trades at $90.38 per barrel, a significant decline of 9.07% within the day, reflecting a broader market sentiment under pressure. This daily drop comes after a pronounced 14-day trend where Brent plummeted from $112.78 to $91.87, representing an 18.5% decrease. Similarly, WTI Crude stands at $82.59, down 9.41%, and gasoline prices are at $2.93, a 5.18% drop. While multiple factors contribute to such market movements, including macroeconomic concerns and supply dynamics, the persistent drumbeat of demand destruction from sectors like public transport electrification adds a foundational bearish pressure that cannot be ignored. Every electric bus on the road, every charging depot constructed, represents a gallon of diesel that will not be consumed, compounding into millions of barrels over time.

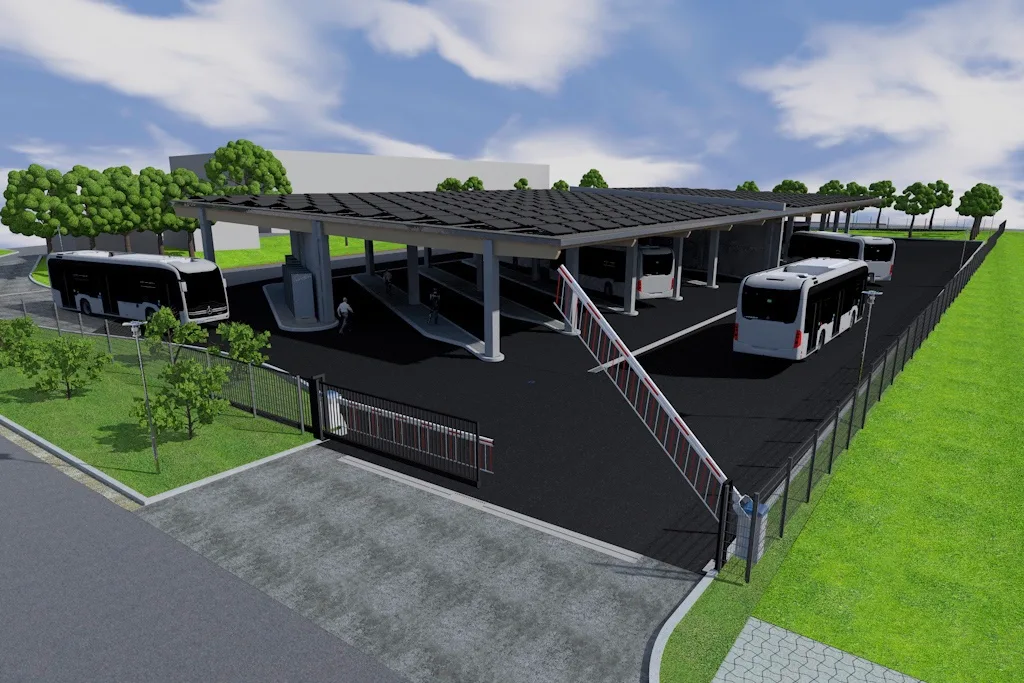

Daimler’s “One-Stop Shop” and the Accelerated Transition

What makes the Regionalbus Leipzig order particularly insightful for investors is not just the shift to electric vehicles, but the comprehensive solution provided by Daimler Buses. Through its subsidiary, Daimler Buses Solutions, the company is offering a “one-stop shop” approach, covering not only the eCitaro buses but also the design and construction of a new e-bus depot, complete with a transformer station, battery storage, photovoltaic system, and ten CCS2 charging points, with an option for 17 more. This integrated approach, which includes the entire infrastructure and charging management system, significantly lowers the barrier to entry for public transport operators considering electrification. By streamlining the transition process and offering tailored solutions, Daimler effectively accelerates the pace at which fleets can convert from diesel to electric. For oil and gas companies, this signals a more rapid erosion of downstream market share than if operators were left to piece together complex infrastructure solutions on their own. The convenience and efficiency of such comprehensive packages will likely spur further adoption, making the electrification of bus fleets a more viable and attractive proposition for municipalities worldwide, ultimately impacting demand for refined products faster than previously anticipated.

Addressing Investor Concerns Amidst a Shifting Energy Paradigm

Our proprietary data indicates that investors are keenly focused on the future trajectory of oil prices, with frequent inquiries such as “What do you predict the price of oil per barrel will be by end of 2026?” and “What are OPEC+ current production quotas?” The Leipzig order, though localized, provides a tangible data point for addressing these broader concerns. The cumulative effect of thousands of such initiatives globally will undoubtedly weigh on future oil demand forecasts. While OPEC+ nations carefully manage supply, their strategies will increasingly need to account for demand-side pressures stemming from accelerated electrification in various sectors. For companies like Repsol, which readers are asking about their performance in April 2026, the energy transition presents both challenges and opportunities. Downstream operations, heavily reliant on fuel sales, face headwinds from reduced consumption, necessitating strategic diversification into renewables, sustainable fuels, or EV charging infrastructure. The long-term price of oil will not only be dictated by geopolitical events and OPEC+ decisions but increasingly by the pace of technological adoption and policy shifts driving electrification, as demonstrated by the Leipzig case. Investors must look beyond immediate headlines to understand these underlying currents shaping the market.

Forward Outlook: Upcoming Events and Strategic Imperatives for Oil & Gas

The implications of electrification initiatives like the one in Leipzig extend directly into the discussions and decisions at upcoming energy events. This weekend, the OPEC+ Joint Ministerial Monitoring Committee (JMMC) on April 18th, followed by the Full Ministerial Meeting on April 19th, will scrutinize global market conditions. While their immediate focus will be on current supply-demand balances and production quotas, the persistent growth of EV fleets, even in the public transport sector, forms a critical backdrop to their long-term strategy. How will OPEC+ adapt its output targets in an environment where demand destruction, however gradual, is a consistent factor? Furthermore, the weekly API and EIA crude inventory reports on April 21st and 22nd, respectively, will offer immediate insights into current stock levels, while the Baker Hughes Rig Count on April 24th will indicate North American production trends. These short-term indicators, when viewed through the lens of long-term demand shifts exemplified by Leipzig, highlight the strategic imperative for oil and gas companies. Investment decisions must increasingly factor in the energy transition, evaluating opportunities in carbon capture, hydrogen, or renewable energy to diversify revenue streams. The path forward for traditional energy companies involves a delicate balance of optimizing hydrocarbon production while strategically investing in the lower-carbon solutions that will define the future energy landscape.