Taiwan’s energy security ambitions have taken a significant step forward with CTCI, a prominent engineering, procurement, and construction (EPC) firm, securing a major $1 billion contract. This latest deal, awarded by state-owned CPC Corporation, focuses on developing a crucial regasification facility at the Kaohsiung Intercontinental LNG Receiving Terminal. This strategic infrastructure investment underscores Taiwan’s commitment to bolstering its natural gas supply resilience, a move with far-reaching implications for its energy landscape and for investors tracking the global LNG sector.

Taiwan’s Strategic LNG Infrastructure Build-Out Accelerates

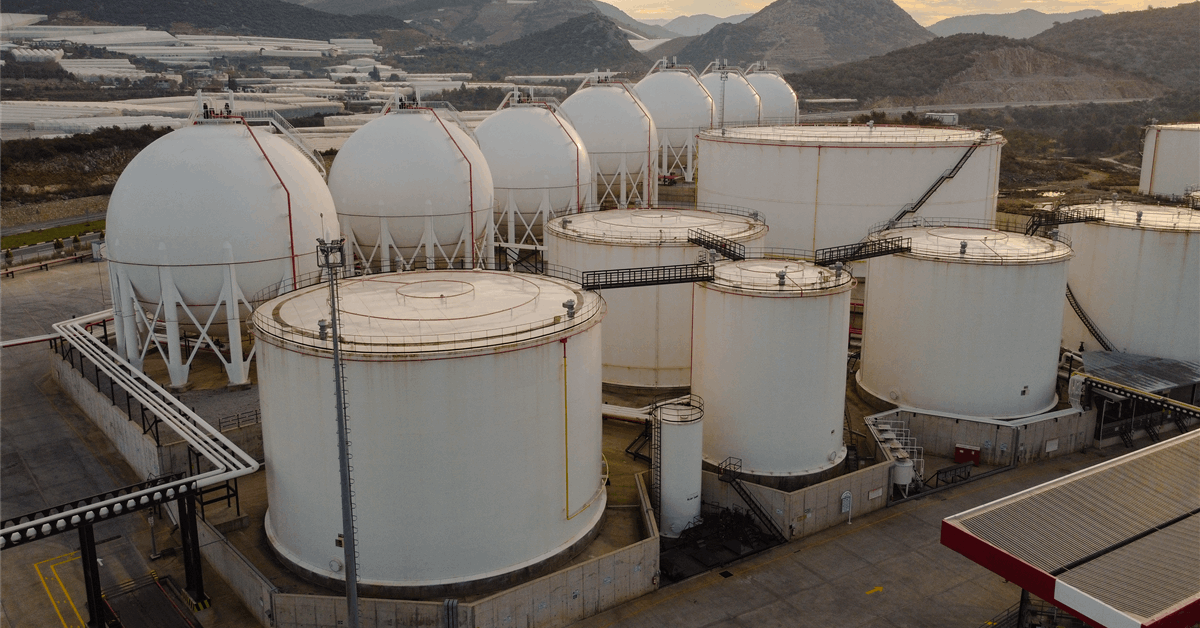

The newly awarded $1 billion (NT 29.6 billion) contract positions CTCI at the heart of Taiwan’s critical energy infrastructure development. The regasification facility at Kaohsiung, slated for completion by 2030, is designed to convert liquefied natural gas (LNG) from four 180,000 kiloliter cryogenic tanks into a gaseous state for island-wide distribution, boasting an impressive output of 1,600 tons per hour. This project is not an isolated effort; CTCI had already secured an LNG storage tanks EPC contract for the same terminal late last year, highlighting a comprehensive, multi-phase development strategy by CPC Corporation. The integration of sustainable and innovative features, such as leveraging seawater for heating and repurposing cold energy for air conditioning, also signals a forward-thinking approach to energy efficiency in large-scale industrial projects.

Beyond Kaohsiung, CTCI’s footprint in Taiwan’s LNG expansion is extensive. Earlier in July, the company clinched another substantial EPC tender, valued at $0.4 billion (NT 12.45 billion), from Formosa Petrochemical Corporation (FPCC). This contract involves building two 160,000 kiloliter cryogenic storage tanks at FPCC’s LNG receiving terminal in the Mailiao Formosa Industrial Complex, Yunlin County. Partnering with Japan’s Kawasaki Heavy Industries (KHI), this project is expected to conclude by mid-2029. Crucially, the LNG stored here will feed new gas-fired power generation units owned by Mai-Liao Power Company, a subsidiary of Formosa Plastics Group, with electricity destined for Taipower, the national provider. These combined projects underscore a robust, multi-pronged effort to secure natural gas for power generation, enhancing national energy independence and stability.

Navigating Volatility: Market Prices and LNG Project Resilience

The backdrop for these significant infrastructure investments is a dynamic and often volatile global energy market. As of today, Brent Crude trades at $90.38, marking a 9.07% decline within the day’s range of $86.08-$98.97. Similarly, WTI Crude stands at $82.59, down 9.41% from its daily high. This intraday dip extends a broader trend, with Brent having fallen by $20.91, or 18.5%, from $112.78 on March 30 to $91.87 just yesterday. While natural gas prices, particularly for LNG cargoes, operate on their own supply-demand fundamentals, crude oil benchmarks often serve as a bellwether for overall energy market sentiment and indirectly influence the cost of energy-intensive projects and the broader financial environment for investment.

For investors, this recent downward pressure on crude prices warrants close observation. While the long-term strategic importance of LNG infrastructure for energy security remains paramount for nations like Taiwan, sustained volatility can influence project financing costs, future gas price assumptions, and the overall investor appetite for capital-intensive ventures. However, the multi-billion-dollar scale and long-term nature of CTCI’s contracts suggest that these projects are underpinned by robust national energy strategies, making them relatively resilient to short-term commodity price fluctuations. The focus here is on securing reliable, long-term energy supply, a driver that often transcends immediate market swings.

Upcoming Catalysts: Shaping the Energy Investment Horizon

Looking ahead, the next two weeks present several critical events that could significantly influence the broader energy market and, by extension, the investment landscape for companies like CTCI and the LNG sector. The most immediate and impactful are the upcoming OPEC+ meetings. The Joint Ministerial Monitoring Committee (JMMC) convenes on Saturday, April 18, followed by the Full Ministerial meeting on Sunday, April 19. These gatherings are pivotal, as any decisions regarding production quotas will directly impact global crude supply and market stability. Investors will be keenly watching for signals on whether the alliance plans to adjust output in response to recent price movements or maintain current levels, a decision that could set the tone for commodity prices in the coming months.

Further insights into market fundamentals will come from the regular inventory reports. The API Weekly Crude Inventory data is due on Tuesday, April 21, and again on April 28, providing an early indication of U.S. crude stocks. These will be followed by the more comprehensive EIA Weekly Petroleum Status Reports on Wednesday, April 22, and April 29, offering detailed U.S. supply, demand, and inventory figures for crude, gasoline, and distillates. Rounding out the supply-side indicators, the Baker Hughes Rig Count will be released on Friday, April 24, and May 1, offering a snapshot of North American drilling activity and future production potential. Collectively, these events provide a crucial roadmap for investors seeking to understand the short-to-medium term trajectory of oil prices and the wider energy sector.

Investor Insights: Addressing Key Questions in the Energy Transition

Our proprietary reader intent data reveals a keen investor focus on long-term oil price predictions and the mechanics of global supply management. Investors are actively asking: “what do you predict the price of oil per barrel will be by end of 2026?” and “What are OPEC+ current production quotas?” These questions underscore the fundamental importance of market forecasting and understanding the levers of supply control in energy investment decisions. Predicting oil prices for the end of 2026 is a complex endeavor, influenced by a multitude of factors ranging from geopolitical developments and global economic growth to the pace of the energy transition and, critically, OPEC+’s strategic responses. While the current Brent price is $90.38, projections for 2026 vary widely, often hinging on assumptions about demand recovery in major economies, the effectiveness of energy transition policies, and the collective discipline of major oil producers.

The question of “OPEC+ current production quotas” directly ties into the upcoming ministerial meetings. Decisions made by this influential group are paramount in setting the global supply ceiling and, consequently, influencing price stability. Understanding their strategy—whether it’s to cut production to support prices, maintain stability, or incrementally increase output—is crucial for any energy investor. For companies like CTCI, while their business is infrastructure development, a stable and predictable energy market environment, even with moderate price levels, fosters greater confidence in long-term project viability and investment returns. These large-scale LNG terminal projects are generational investments, less sensitive to daily commodity swings but highly dependent on the strategic vision of nations prioritizing energy security and the broader economic stability that underpins such massive capital outlays. Taiwan’s proactive stance, backed by CTCI’s proven EPC capabilities, positions it well in this evolving energy landscape.