The Evolving Risk Landscape: Climate Resilience Meets Oil & Gas Investment

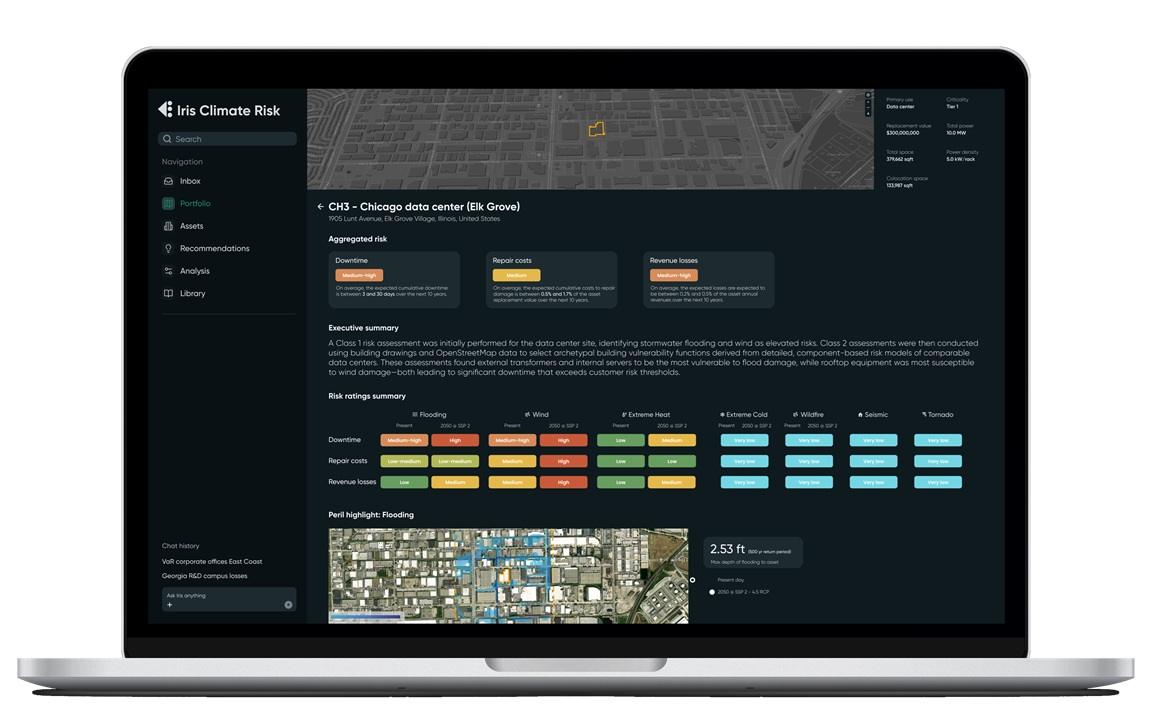

The recent announcement of Class 3 Technologies securing $3.5 million in seed funding for its advanced climate risk modeling software, Iris, signals a critical juncture in how capital markets are beginning to assess and price physical climate risks. While Iris specifically targets the built environment, its underlying engineering-based approach to quantifying vulnerabilities at an individual asset level carries profound implications for the broader energy sector. For oil and gas investors, this development underscores an accelerating trend: the convergence of traditional market fundamentals with an increasing emphasis on asset resilience, ESG metrics, and the long-term viability of infrastructure in a climate-challenged world. Understanding this pivot is no longer a peripheral concern but central to robust investment strategy, influencing everything from insurance premiums and operational costs to regulatory compliance and shareholder value.

Navigating Volatility: A Bearish Wind Sweeps Through Crude Markets

The imperative for sophisticated risk assessment is particularly acute given the current volatility in energy markets. As of today, Brent Crude trades at a notable $90.38 per barrel, marking a sharp 9.07% decline from its previous close. This significant downturn is mirrored in WTI Crude, which has fallen to $82.59, down 9.41%, with U.S. gasoline prices following suit at $2.93, a 5.18% drop. This recent dip is not an isolated event; our proprietary data reveals that Brent has shed a substantial $22.4, or nearly 20%, over the past two weeks alone, plummeting from $112.78 on March 30th to its current level. Such dramatic swings directly impact the earnings potential and cash flow generation of oil and gas producers, making it harder to justify capital-intensive projects, including those aimed at improving climate resilience. The ability to accurately model and mitigate physical risks, as pioneered by Class 3, could offer a crucial competitive edge by providing a clear return on investment for resilience measures, even in a challenging price environment.

Investor Focus: Supply Dynamics, Future Prices, and Data-Driven Foresight

Our proprietary reader intent data this week reveals a keen focus among investors on the trajectory of crude prices and the influence of major supply-side players. Investors are actively questioning the potential for oil prices by the end of 2026, a clear indication that current volatility is prompting a re-evaluation of long-term forecasts and risk exposure. Similarly, queries regarding OPEC+’s current production quotas highlight the market’s continued reliance on coordinated supply management to stabilize prices. These questions underscore a fundamental truth for energy investors: the need for robust, data-driven insights to navigate complex market dynamics. The emergence of precise climate risk modeling tools, like Iris, aligns with this demand for granular data, extending the concept of “data-driven decisions” beyond traditional supply-demand metrics to encompass environmental and physical threats to asset value. As investors increasingly seek transparency and predictive power, the integration of climate risk into financial models will become as critical as understanding geopolitical supply disruptions.

Key Catalysts on the Horizon: OPEC+ Decisions and Inventory Shifts

The immediate market outlook hinges on several critical events scheduled for the coming days, which will undoubtedly influence short-term price movements and investor sentiment. The OPEC+ Joint Ministerial Monitoring Committee (JMMC) meeting on April 19th, followed by the full Ministerial Meeting on April 20th, will be paramount. Given the recent significant price decline in crude, market participants will be keenly watching for any signals regarding adjustments to production quotas or reaffirmation of current cuts. Any deviation from expectations could trigger further volatility. Further insights into supply-demand balances will come from the API Weekly Crude Inventory report on April 21st and the EIA Weekly Petroleum Status Report on April 22nd. These reports, coupled with the Baker Hughes Rig Count on April 24th, will provide crucial data points on U.S. production activity and inventory builds, directly impacting short-term price sentiment. Over the subsequent week, another round of API and EIA reports (April 28th and 29th, respectively) and the Baker Hughes Rig Count (May 1st) will continue to shape market perceptions. These near-term events, while focused on traditional market fundamentals, also indirectly influence the ability of energy companies to allocate capital towards long-term resilience initiatives. A strong price environment offers greater flexibility for investment in climate adaptation, while prolonged weakness could force difficult trade-offs.

Strategic Implications for Oil & Gas Investment

The $3.5 million investment in Class 3 Technologies is more than just a seed round for a software startup; it’s a bellwether for the evolving landscape of risk and value in physical assets. For oil and gas investors, this trend mandates a broadened perspective that integrates both immediate market signals – like the recent sharp decline in Brent crude and the upcoming OPEC+ deliberations – with the long-term, structural shifts driven by climate change. As companies like Class 3 develop tools to quantify specific climate vulnerabilities, the pressure on energy firms to assess, disclose, and mitigate these risks will only intensify. Investment decisions in the energy sector must increasingly account for the resilience of assets against extreme weather events, the cost of insurance, and the expectations of a growing pool of ESG-conscious capital. The future of energy investment demands a holistic view, where financial performance is inextricably linked to environmental stewardship and robust climate risk management.