The global energy landscape continues its dynamic evolution, presenting both formidable challenges and compelling opportunities for astute oil and gas investors. As the industry grapples with the dual imperatives of energy security and decarbonization, innovative strategies are no longer optional but essential for sustainable growth. Against this backdrop, the convergence of carbon capture, utilization, and storage (CCUS) with circular economy principles is emerging as a powerful nexus, transforming what was once considered a cost burden into a significant value-creation pathway. For investors navigating this complex transition, understanding how captured carbon can be integrated into resource-efficient systems is key to identifying the next generation of resilient, high-performing energy assets.

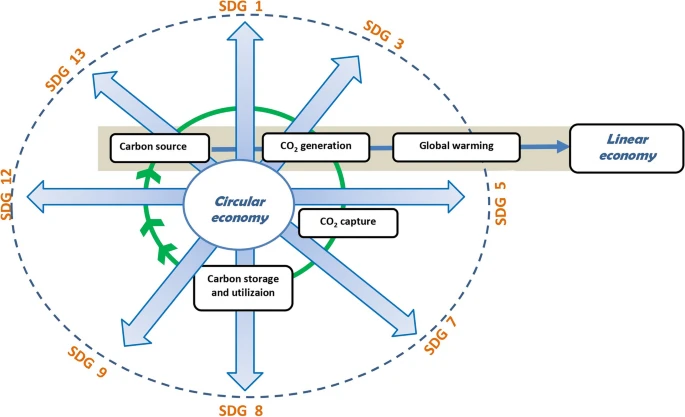

The Circular Economy: Unlocking New Value Streams from Carbon

Traditional industrial models, characterized by a ‘take, make, dispose’ approach, are increasingly unsustainable. The circular economy paradigm, however, champions resource efficiency, waste minimization, and the continuous reuse and recycling of materials. When applied to carbon capture, this framework fundamentally shifts the perception of CO2 from a liability to a valuable feedstock. Rather than simply sequestering carbon, the circular approach emphasizes its transformation into tangible, marketable products. This includes the production of vital chemicals, sustainable construction materials, and even synthetic fuels, alongside agricultural inputs like fertilizers and advanced bio-based plastics. For companies in the oil and gas sector, this integration represents a strategic pivot, allowing them to diversify revenue streams, reduce reliance on virgin raw materials, and enhance their environmental, social, and governance (ESG) credentials. The economic multiplier effect of such synergy is significant, fostering innovation, creating green jobs, and building industrial resilience against future resource shocks.

Navigating Market Volatility with Diversified Carbon Investments

The current market environment underscores the urgent need for diversified and resilient investment portfolios. As of today, Brent crude trades at $90.38, reflecting a notable decline of 9.07% within the day, with a range between $86.08 and $98.97. Similarly, WTI crude has seen a substantial drop of 9.41% to $82.59, moving within a day range of $78.97 to $90.34. This sharp downturn comes on the heels of a significant 14-day trend where Brent crude shed nearly 20% of its value, falling from $112.78 on March 30th to today’s levels. Such volatility, also mirrored in gasoline prices currently at $2.93, down 5.18%, highlights the inherent risks of over-reliance on traditional fossil fuel commodities. Investors are rightly asking about the trajectory of crude prices by the end of 2026, seeking clarity amid the fluctuations. Investing in carbon capture projects integrated into a circular economy offers a crucial hedge. By deriving value from CO2 conversion, companies can generate returns less susceptible to the immediate swings of crude oil prices, providing a more stable and predictable cash flow stream that appeals to long-term capital.

Policy Catalysts and Upcoming Events Shaping Carbon Investment

The successful scaling of circular economy-integrated carbon solutions hinges significantly on supportive policy frameworks, robust government incentives, and cross-sector collaboration. These elements are critical for overcoming initial technical and financial hurdles. The broader energy market dynamics, influenced by key upcoming events, also play an indirect yet significant role in shaping the investment landscape for decarbonization technologies. For instance, the OPEC+ JMMC Meeting on April 19th and the subsequent OPEC+ Ministerial Meeting on April 20th will set the tone for global crude supply. While these meetings directly impact crude prices, the outcomes will influence the overall investment sentiment in the energy sector. A tighter supply scenario, for example, could drive higher fossil fuel prices, paradoxically making the cost of carbon emissions more pronounced and bolstering the economic case for CCUS. Furthermore, the regular updates from the API Weekly Crude Inventory on April 21st and 28th, alongside the EIA Weekly Petroleum Status Reports on April 22nd and 29th, provide vital snapshots of market health. These reports, combined with the Baker Hughes Rig Count on April 24th and May 1st, offer critical data points that inform investor decisions, reinforcing the necessity for energy companies to future-proof their operations through sustainable innovation. Investors are keenly watching OPEC+ production quotas, understanding that these decisions ripple through the entire energy value chain, influencing the urgency and viability of carbon reduction investments.

Identifying Opportunities in the Carbon-to-Value Frontier

The shift towards a circular carbon economy presents diverse investment opportunities across various technological and industrial applications. Beyond simply storing CO2 in geological formations or considering ocean storage – each with its own advantages and challenges – the direct utilization of captured carbon is gaining traction. Mineral carbonation, for example, transforms CO2 into stable solid materials that can be incorporated into construction, offering a permanent sequestration solution while simultaneously supporting circular resource flows in industries like cement and aggregates. This innovative approach aligns perfectly with the growing demand for sustainable building materials and low-carbon infrastructure. Investors are increasingly seeking detailed insights into the data sources powering market analysis, indicating a strong appetite for robust, forward-looking intelligence to pinpoint these emerging sectors. Companies that proactively invest in research, development, and commercial deployment of these carbon-to-value technologies are poised for significant long-term gains. Their ability to generate economic value from waste, secure resource efficiency, and meet increasingly stringent sustainability mandates will differentiate them in a competitive market. As such, while some investors might be focused on the near-term performance of individual players like Repsol, the strategic long-term outperformance will likely belong to those entities fundamentally integrating circularity into their core business models, transforming environmental challenges into profitable opportunities.