The global drive towards decarbonization continues to reshape investment landscapes across the energy sector, pushing capital into innovative solutions that address high-emission industries. Among these, cement production stands out as a significant contributor to global CO2 emissions, presenting both a formidable challenge and a burgeoning opportunity for pioneering technologies. Our analysis at OilMarketCap.com highlights a compelling avenue for investment within Carbon Capture, Utilization, and Storage (CCUS) strategies: the integration of advanced biochar into building materials. This approach promises not only to mitigate the cement industry’s environmental footprint but also to enhance material performance, signaling a potent long-term value proposition for discerning investors.

Cement’s Carbon Conundrum and the Biochar Breakthrough

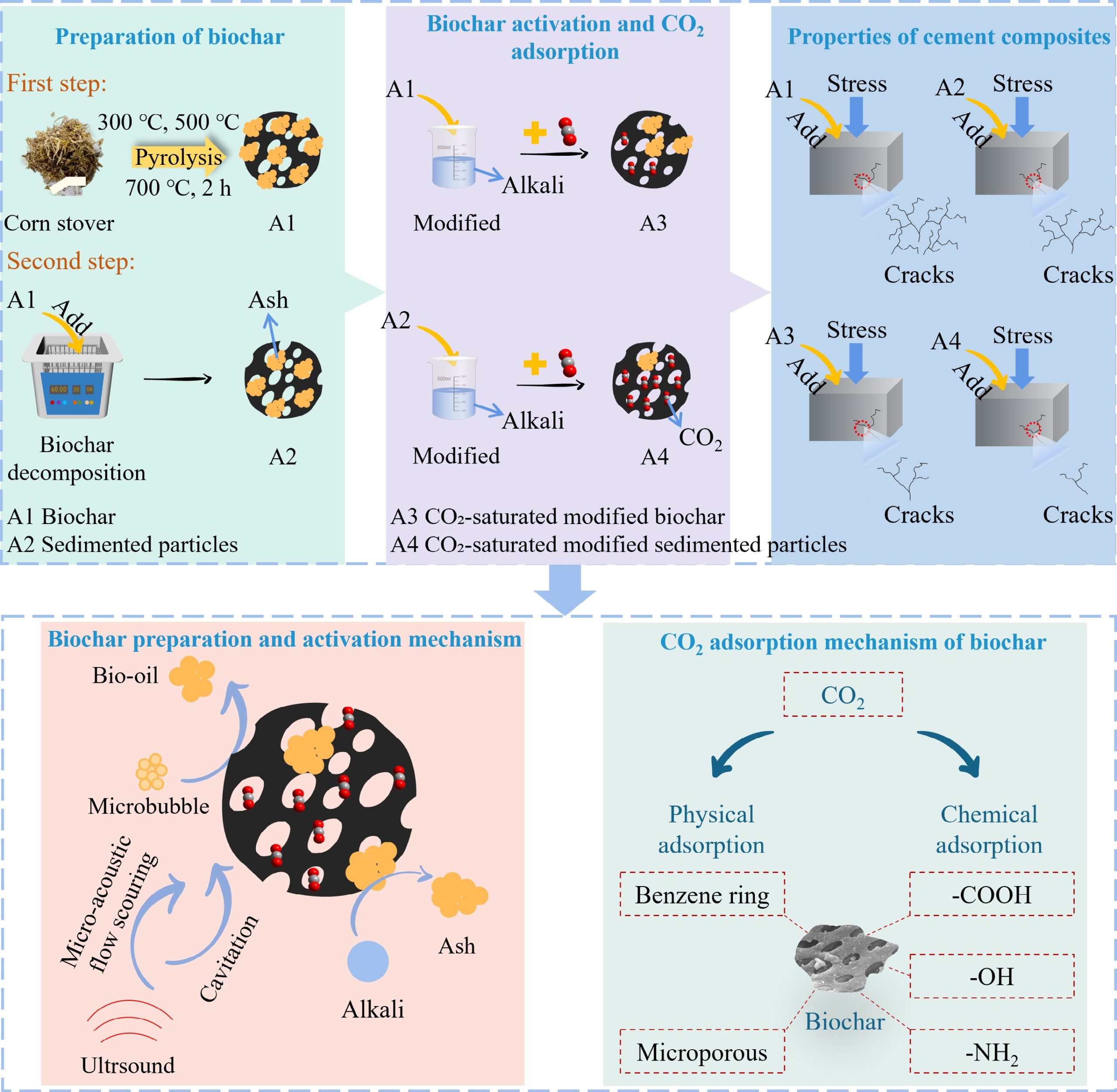

The imperative to decarbonize heavy industries is undeniable, with cement manufacturing alone responsible for a substantial portion of global CO2 output. Traditional methods of emission reduction have often focused on operational efficiencies or post-combustion capture. However, new research points to a more integrated solution: transforming the very material itself into a carbon sink. Scientists have explored the potential of modifying biochar, a porous, carbon-rich material derived from plant waste, to make cement significantly more sustainable.

The foundational research involved producing biochar from corn straw at varying temperatures, isolating specific sedimented particles, and then treating both original and separated samples with an alkali solution. This treatment was critical for enhancing the material’s microscopic pore structure, thereby improving its CO2 adsorption capacity. The findings are particularly encouraging: biochar produced at 500 °C demonstrated superior overall performance, effectively combining robust CO2 adsorption with improved cement characteristics. When integrated into cement, especially at a one percent replacement level, the CO2-saturated modified biochar resulted in a denser, stronger material. This dual benefit—enhanced mechanical strength alongside a reduced total carbon footprint—underscores biochar’s potential to transform ordinary cement into a carbon-storing building block without compromising structural integrity. This innovation represents a practical step toward greener construction, offering a scalable solution for an industry in critical need of decarbonization.

Navigating Market Volatility: CCUS as a Strategic Hedge

In a global energy market characterized by persistent volatility, strategic diversification becomes paramount for investors. As of today, April 19, 2026, Brent crude trades at $90.38 per barrel, a notable decline of 9.07% within the day, with its range fluctuating significantly between $86.08 and $98.97. Similarly, WTI crude stands at $82.59, down 9.41%. This sharp daily contraction follows a broader trend; Brent has seen a substantial drop from $112.78 on March 30 to its current level, representing a 19.9% decrease in just over two weeks. Such price swings, coupled with gasoline prices at $2.93 and down 5.18%, underscore the unpredictable nature of traditional hydrocarbon markets.

Against this backdrop, investments in CCUS technologies, particularly those integrated into high-volume industries like cement, offer a compelling long-term value proposition that is largely decoupled from the immediate ebbs and flows of crude prices. While energy sector investments have historically been tethered to commodity cycles, the accelerating energy transition and increasing regulatory pressures are creating new, more stable growth vectors. Deploying capital into sustainable materials like biochar-enhanced cement provides a hedge against commodity price volatility, aligning portfolios with the structural demand for decarbonization solutions. Companies leading in such innovations are positioning themselves for resilient growth, appealing to a broader investor base focused on both financial returns and environmental, social, and governance (ESG) metrics.

Investor Focus Shifts: Beyond Short-Term Crude to Long-Term Value

Our proprietary reader intent data at OilMarketCap.com reveals a strong, consistent investor focus on the near-term dynamics of crude markets. A significant portion of inquiries centers on “what do you predict the price of oil per barrel will be by end of 2026?” and “What are OPEC+ current production quotas?” These questions highlight the immediate concerns around supply-demand balances and the potential for short-term gains or losses in traditional oil and gas equities. Furthermore, interest in the performance of integrated majors like Repsol reflects a desire to understand how established players are navigating the current environment.

However, forward-thinking investors are increasingly recognizing that while these questions are critical for tactical trading, the strategic long-term value lies in understanding and investing in the structural shifts underpinning the energy transition. The cement industry’s decarbonization, facilitated by innovations like biochar CCUS, represents a multi-decade opportunity that is less influenced by daily OPEC+ decisions or weekly inventory reports. Instead, its drivers are regulatory mandates, corporate sustainability targets, and the fundamental need for cleaner infrastructure. Investors who broaden their perspective beyond just crude price forecasts to consider the immense market potential of carbon-storing materials are positioning themselves to capitalize on the next wave of energy sector growth, tapping into markets that offer predictable demand and significant societal impact.

Upcoming Catalysts and the Broader CCUS Investment Horizon

While the immediate energy calendar is populated with events that will undoubtedly sway traditional oil markets—such as the OPEC+ Joint Ministerial Monitoring Committee (JMMC) Meeting on April 19, followed by the Ministerial Meeting on April 20, and recurring API and EIA weekly crude inventory reports on April 21/22 and April 28/29—the catalysts for CCUS investment operate on a different timeline and scale. These traditional events dictate short-term supply and sentiment, but they also underscore the ongoing pressures for the energy sector to diversify and innovate.

For CCUS, the key drivers are not daily inventory changes but rather evolving policy frameworks, increasing carbon pricing mechanisms, and ambitious corporate net-zero commitments. The development of cost-effective, scalable solutions like biochar in cement, which simultaneously enhance material properties and sequester CO2, will be crucial. Upcoming government policy announcements, national infrastructure bills, and corporate ESG reporting cycles will serve as significant catalysts for CCUS adoption. Investors should monitor developments in material science patents, venture capital funding rounds for green construction technologies, and partnerships between energy majors and sustainable material innovators. The long-term investment horizon for CCUS in heavy industry, while not tied to specific weekly reports, is bolstered by an irreversible global commitment to reduce emissions, making these technologies a critical component of any forward-looking energy portfolio.