The distant image of melting glaciers in California’s Sierra Nevada might seem far removed from the daily machinations of global energy markets, yet for astute oil and gas investors, it serves as a stark, tangible bellwether. New research highlighting the unprecedented and rapid disappearance of these ancient ice formations, some dating back tens of thousands of years, underscores the accelerating pace of climate change. This scientific reality is not merely an environmental concern; it is a critical, increasingly quantifiable risk factor and a driver of opportunity within the energy sector, influencing everything from regulatory frameworks and capital allocation to long-term demand projections and investor sentiment. Understanding how these macro climate trends translate into micro investment decisions is paramount for navigating the evolving landscape of oil and gas.

Climate Bellwethers and Long-Term Energy Outlook

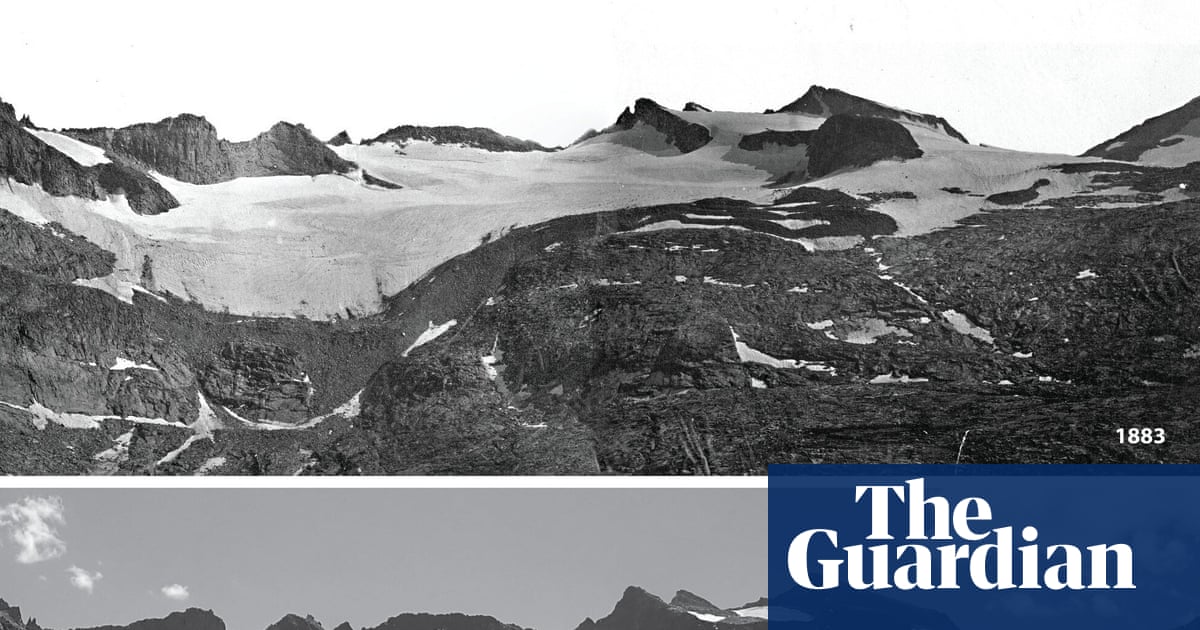

The profound scientific findings regarding the Sierra Nevada’s glaciers – specifically the Conness, Maclure, Lyell, and Palisade glaciers – illustrate a future where peaks that have been ice-covered for millennia will be bare for the first time in human history. This isn’t just an ecological shift; it’s a powerful symbol of the climate crisis’s escalating impact. For oil and gas investors, such developments amplify the pressure for decarbonization and accelerate the energy transition. Many of our readers are asking about the long-term trajectory of crude prices, with a recurring question being, “What do you predict the price of oil per barrel will be by end of 2026?” While short-term volatility is constant, the pace of climate change, exemplified by these melting glaciers, directly influences the policy environment, technology adoption, and ultimately, the future demand curve for hydrocarbons. Governments and international bodies are increasingly likely to implement more stringent emissions targets, carbon pricing mechanisms, and incentives for renewable energy. This translates to potential long-term demand destruction for fossil fuels, making the forward-looking strategy of energy companies, and therefore their investment appeal, inextricably linked to their transition plans.

Market Dynamics Amidst Climate Uncertainty

Current market movements reflect a complex interplay of immediate supply-demand factors and broader long-term concerns, including those stemming from climate change narratives. As of today, Brent Crude trades at $90.38, reflecting a significant 9.07% decline, with its daily range stretching from $86.08 to $98.97. Similarly, WTI Crude has fallen to $82.59, down 9.41% on the day, moving between $78.97 and $90.34. Gasoline prices have also seen a drop to $2.93, a 5.18% decrease. This recent downturn follows a notable trend, with Brent having shed $22.4, or 19.9%, over the past 14 days from its $112.78 perch on March 30th. While immediate factors like inventory data or geopolitical shifts often drive such sharp daily and weekly movements, this volatility is increasingly underscored by investor apprehension regarding future demand. The narrative around accelerating climate change, reinforced by scientific reports of glacier melt and other environmental indicators, contributes to a sentiment where peak oil demand might arrive sooner than previously anticipated. This perception, whether fully realized or not, impacts hedging strategies, investment horizons, and the overall risk premium associated with oil and gas assets.

Navigating Immediate Catalysts and Strategic Shifts

Even as the long-term shadow of climate risk lengthens, immediate market catalysts continue to drive short-term trading decisions and operational adjustments. Investors are keenly focused on events that can move the needle on supply, demand, and pricing in the coming weeks. The upcoming OPEC+ Ministerial Meeting on April 19th is a prime example, where decisions on production quotas will directly impact global crude supply. Many of our readers are asking, “What are OPEC+ current production quotas?” and how these might shift. Following this, the API Weekly Crude Inventory report on April 21st and the EIA Weekly Petroleum Status Report on April 22nd will provide crucial insights into U.S. supply and demand dynamics, typically moving prices in the immediate aftermath. The Baker Hughes Rig Count on April 24th offers a glimpse into future production capacity. However, even these seemingly tactical events are now viewed through a strategic lens. OPEC+ decisions, for instance, are not solely about market share but increasingly consider the evolving energy landscape and the long-term implications of aggressive climate policies on future oil demand. Companies reporting strong financials while also demonstrating credible decarbonization strategies are likely to attract more capital, highlighting a fundamental shift in what constitutes a “safe” or “growth” investment in the energy sector.

Capital Allocation and the Decarbonization Imperative

The scientific evidence of accelerating climate change, exemplified by the rapid melt of California’s ancient glaciers, places an unequivocal imperative on oil and gas companies to adapt their capital allocation strategies. Investors are no longer content with mere pledges; they demand concrete action and transparent reporting on emissions reductions, investments in cleaner energy, and the development of sustainable business models. Companies that fail to pivot risk becoming stranded assets in a decarbonizing world. This means scrutinizing capital expenditures for new exploration and production projects, especially those with high carbon intensity, and favoring those that integrate carbon capture, utilization, and storage (CCUS) or align with renewable energy development. The flow of investment capital is increasingly being redirected towards firms demonstrating genuine commitment to the energy transition, whether through significant investments in wind, solar, geothermal, or advanced biofuels. This strategic shift is not just about environmental responsibility; it’s about financial resilience and securing long-term value in a global economy increasingly shaped by climate realities. Understanding a company’s pathway to net-zero, its investments in emerging energy technologies, and its capacity to manage regulatory and reputational risks is now as critical as evaluating its reserve replacement ratio or production efficiency.