The recent delivery of the “Alexey Kosygin,” Russia’s first domestically built Arc-7 ice-class tanker, marks a pivotal moment for the Novatek PJSC-led Arctic LNG 2 project. This event signals a renewed, albeit challenging, push by Russia to bolster its liquefied natural gas export capacity amidst persistent international sanctions. For global energy investors, this development is more than just a logistical milestone; it represents a critical indicator of Russia’s resilience in the face of geopolitical headwinds, its strategic pivot towards Asian markets, and the intricate balance of supply-side factors that continue to shape the volatile landscape of oil and gas. Understanding the operational implications and the broader market context of this delivery is essential for navigating investment decisions in a sector increasingly defined by supply chain vulnerabilities and shifting trade alliances.

Arctic LNG 2: Navigating the Ice and Sanctions Barrier

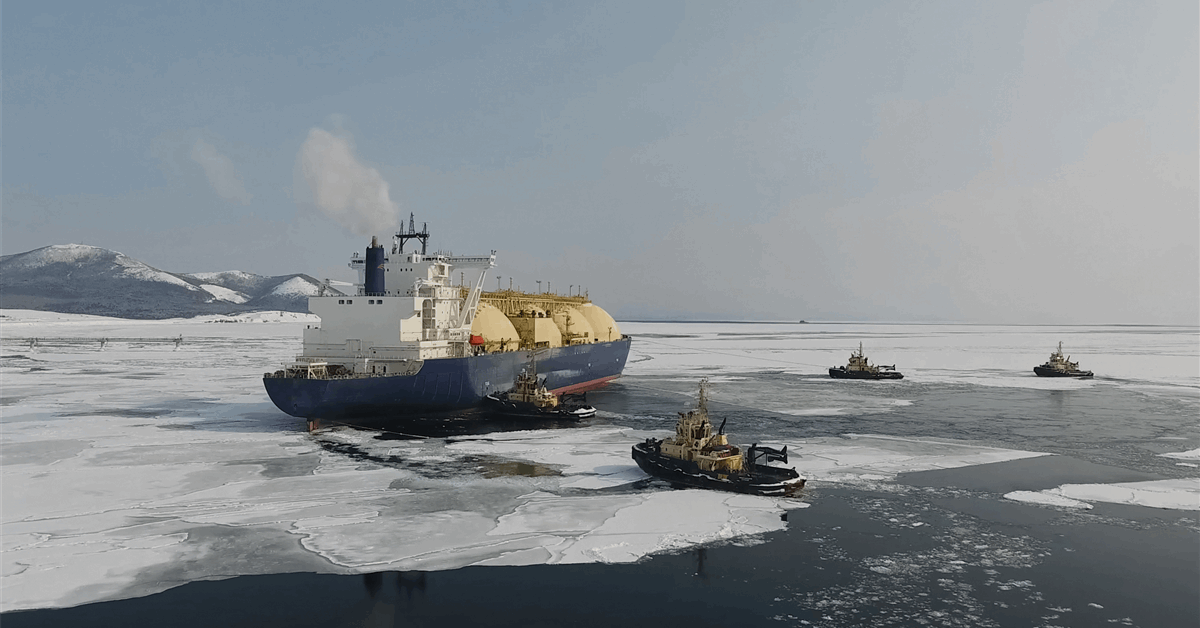

The “Alexey Kosygin” is not merely another vessel; it is a strategic asset designed to unlock year-round navigation through the treacherous Northern Sea Route, a lifeline for the Arctic LNG 2 project. Before this delivery, the project relied heavily on non-ice-class tankers for much of the year, with only one identified advanced Arc-7 class tanker, the “Christophe de Margerie,” capable of operating in heavy winter ice. The initial expectation for the “Alexey Kosygin’s” delivery was early 2023, but equipment supply restrictions, a direct consequence of international sanctions, caused significant delays. This operational hurdle directly impacted the project’s ability to maintain consistent output, forcing cuts as winter ice thickened. The integration of this new icebreaker-class vessel, with two more expected from the Zvezda Shipbuilding Complex next year, according to Sovcomflot’s CEO, Igor Tonkovidov, promises to enhance the project’s export reliability. However, the path remains fraught, as the overall fleet needed to service the ambition of tripling Russia’s super-chilled fuel production by the end of the decade still faces considerable expansion challenges due to ongoing Western restrictions.

China’s Crucial Role and Shifting Global LNG Dynamics

While sanctions have constrained Arctic LNG 2’s development and fleet expansion, China has emerged as a critical enabler for the project’s viability. The Asian nation began importing fuel from Arctic LNG 2 through its remote Beihai terminal last August, with approximately 20 cargoes offloaded by mid-December. This consistent demand from China provides a much-needed outlet for Russian LNG, helping to mitigate the impact of Western market exclusions. For investors, China’s commitment is a key de-risking factor, offering a clear signal that a significant portion of the project’s output has a guaranteed buyer. This strategic alliance underscores the evolving geopolitical landscape of energy trade, where traditional supply routes are being re-routed and new partnerships forged. The increasing flow of Russian LNG to China, facilitated by vessels like the “Alexey Kosygin,” could exert downward pressure on global natural gas prices over the long term, potentially altering the competitive dynamics for other LNG producers and exporters. Investors should closely monitor Chinese demand signals and future import agreements as critical drivers for the project’s ultimate success.

Market Realities and Investor Outlook Amidst Volatility

The broader energy market currently presents a complex picture for investors, with crude benchmarks reflecting recent volatility. As of today, Brent Crude trades at $89.95, down 0.53% within a daily range of $93.87 to $95.69. Similarly, WTI Crude stands at $86.28, having dropped 1.3% within its day range of $85.5 to $87.47. This snapshot follows a significant downward trend for Brent, which has fallen by $23.49, or 19.8%, from $118.35 on March 31st to $94.86 on April 20th. Many investors are keenly asking about the immediate direction of WTI and what to predict for oil prices by the end of 2026. The current weakness is influenced by various factors, including global demand concerns and an evolving supply landscape. While the “Alexey Kosygin” directly impacts LNG, its successful operation contributes to a more robust Russian energy export capacity, indirectly influencing the broader sentiment in energy markets. Investors must consider how increased, albeit sanctioned, Russian energy flows, whether crude or LNG, contribute to overall global supply, potentially capping upward price movements. The interplay between geopolitical tensions, production discipline from OPEC+, and the resilience of projects like Arctic LNG 2 will dictate the trajectory for crude and natural gas prices in the coming quarters.

Forward Momentum: Key Events Shaping the Near-Term

Looking ahead, several critical events on the energy calendar will provide further clarity and potential catalysts for market movements, directly impacting investor strategies. Today, April 21st, the OPEC+ JMMC Meeting is underway, where key producers discuss market conditions and compliance with output agreements. Any signals regarding future supply adjustments could significantly sway crude prices. Tomorrow, April 22nd, and again on April 29th, the EIA Weekly Petroleum Status Reports will offer vital insights into U.S. crude inventories, refinery activity, and demand indicators, providing a real-time pulse on the world’s largest consumer. The Baker Hughes Rig Count on April 24th and May 1st will shed light on North American drilling activity, hinting at future domestic supply. Perhaps most crucial for investors seeking longer-term guidance, the EIA Short-Term Energy Outlook on May 2nd will publish updated forecasts for global supply, demand, and prices, directly addressing the prevalent investor question about end-of-year price predictions. These upcoming data points, combined with continued developments around projects like Arctic LNG 2, will be instrumental in shaping market sentiment and refining investment theses for the remainder of 2026.