The global energy landscape continues its relentless evolution, underscoring the critical role of strategic infrastructure development in securing future supply. In a significant move for the Australian market, AG&P LNG, backed by Florida-based Nebula Energy, has finalized its agreement to acquire Venice Energy’s proposed LNG import terminal in South Australia. This acquisition, culminating from negotiations initiated last October, positions AG&P LNG to become a pivotal player in Australia’s efforts to enhance energy security and address looming gas supply shortfalls. For investors, this development signals a clear commitment to long-term energy solutions amidst fluctuating commodity markets and offers a compelling case study in value creation through timely infrastructure deployment.

Addressing Australia’s Looming Gas Deficit

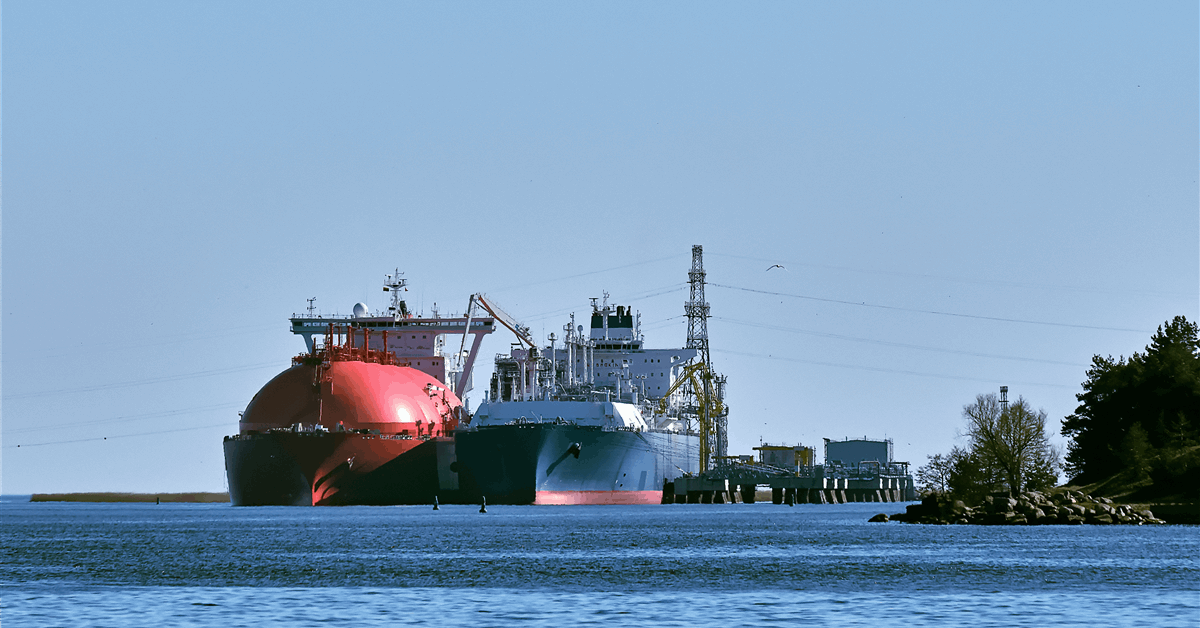

The strategic importance of the South Australian LNG project cannot be overstated. With a final investment decision (FID) anticipated this year, the Outer Harbor LNG import terminal is poised to provide crucial energy security to South Australia from 2028 onwards. The project directly targets forecast gas supply shortfalls across the southeast of Australia, a challenge that has increasingly concerned policymakers and energy operators. Venice Energy’s chairman highlighted the terminal’s capacity to deliver approximately 60 PJs per year directly to the Iona underground gas storage facility via the 687-kilometer SEA Gas pipeline, with an additional 30 PJs slated for the Port Campbell pipeline. This direct link to vital storage and distribution networks significantly enhances the project’s value proposition, particularly in light of the recently announced 25-year agreement between Snowy Hydro and Lochard Energy for gas storage at Iona. The ability to strategically store and deploy gas to power stations will be instrumental in preventing potential state-wide blackouts as domestic gas supplies continue to decline.

AG&P LNG’s decision to acquire a “shovel-ready” project with all key permits already in place offers a distinct competitive advantage. This significantly de-risks the development timeline and expedites the path to commercial operation, differentiating it from other potential LNG import terminal proposals in the region that may still face regulatory hurdles and site preparation challenges. The planned conversion of a 145,000 cbm LNGC into a Floating Storage and Regasification Unit (FSRU) with a peak send-out capacity of 400 mmscfd further underscores an efficient, capital-light approach to bringing essential infrastructure online quickly.

Navigating Volatile Markets: Project Valuation in a Dynamic Environment

For investors assessing the long-term value of such infrastructure projects, understanding current market dynamics is paramount. As of today, Brent crude trades at $98.63 per barrel, marking a respectable 3.9% gain for the day, with WTI crude following suit at $90.51, up 2.7%. Gasoline prices also reflect this upward movement, standing at $3.08, a 2.66% increase. However, a broader look at the past fortnight reveals a more nuanced picture for crude, with Brent experiencing a notable decline of 12.4%, falling from $108.01 on March 26th to $94.58 on April 15th before today’s rebound. This recent volatility underscores the importance of resilient, long-term energy assets like the Outer Harbor LNG terminal.

Investors frequently inquire about the drivers behind Asian LNG spot prices and the consensus Brent forecast for 2026. While short-term spot prices can be influenced by immediate demand surges, weather events, or supply disruptions, projects like AG&P LNG’s Australian terminal provide foundational supply that can help stabilize regional markets over the long haul. By adding a reliable source of regasified LNG, it mitigates the impact of global supply chain shocks and enhances energy security, indirectly influencing pricing stability. The current crude price movements, though volatile, generally reflect a tight market, a backdrop that supports continued investment in gas infrastructure as a transition fuel and a critical component of energy mixes globally. Long-term Brent forecasts, which investors are keenly tracking, will ultimately factor in the success of such projects in balancing supply and demand.

AG&P LNG’s Strategic Expansion and Investor Confidence

The acquisition of Venice Energy marks AG&P LNG’s strategic entry into the Australian market, a move consistent with its broader global vision. Majority-owned by Florida-based Nebula Energy, AG&P LNG brings extensive experience in developing and operating LNG infrastructure. Their choice to acquire an advanced-stage project rather than initiating a greenfield development highlights a pragmatic and efficient strategy to accelerate market penetration. The use of an FSRU conversion is a testament to this approach, allowing for quicker deployment compared to land-based terminals and often at a lower capital expenditure.

This expansion aligns with the increasing global recognition of LNG as a crucial bridge fuel and a key component of future energy portfolios, especially for nations seeking to reduce reliance on more carbon-intensive alternatives while ensuring energy reliability. For investors tracking the footprint of major energy players, AG&P LNG’s move into a mature, stable market like Australia, with strong government backing for energy security initiatives, enhances its profile as a growth-oriented entity in the LNG sector. This strategic positioning could attract further capital and partnerships as the project progresses towards its FID and subsequent operational phases.

Forward Outlook: Key Catalysts and Investor Focus Areas

Looking ahead, the energy market is replete with upcoming events that will continue to shape investor sentiment and commodity price trajectories. In the immediate future, key industry data points such as the Baker Hughes Rig Count on April 17th and 24th will provide insights into drilling activity. More significantly, the OPEC+ Joint Ministerial Monitoring Committee (JMMC) meeting on April 18th, followed by the full Ministerial Meeting on April 20th, will be closely watched for any signals regarding production policy. Decisions from these meetings directly influence global crude supply, impacting the broader energy complex including natural gas and LNG pricing.

Furthermore, the API Weekly Crude Inventory reports on April 21st and 28th, along with the EIA Weekly Petroleum Status Reports on April 22nd and 29th, will offer critical insights into U.S. supply and demand dynamics. These reports are instrumental for investors building a base-case Brent price forecast for the next quarter, a frequent query among our readers. The combined intelligence from these events will help refine the consensus 2026 Brent forecast and provide context for the long-term viability and profitability of major energy infrastructure projects like the South Australian LNG terminal. As the project moves towards its FID this year, these macroeconomic signals will play a crucial role in securing financing and off-take agreements, underscoring the interconnectedness of global energy markets and localized infrastructure development.