The Strait of Hormuz Reopening: A Fleeting Relief or a Fundamental Shift for Oil Markets?

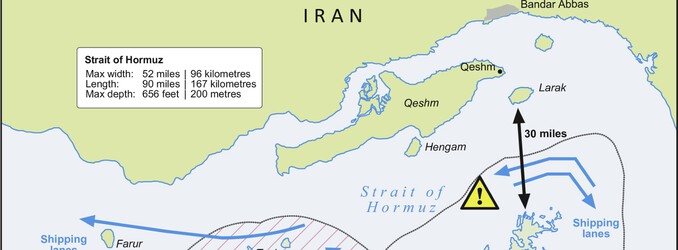

The global oil market experienced a seismic shift this week as Iran announced the full reopening of the Strait of Hormuz to commercial shipping, a critical artery for over one-fifth of the world’s oil and LNG flows. This development, linked to a tenuous 10-day ceasefire between Israel and Hezbollah, initially triggered a sharp sell-off in crude prices, signaling immediate relief from the supply bottlenecks that have plagued the market since the strait’s effective closure in late February. However, a deeper dive into current market dynamics and underlying geopolitical tensions reveals a more complex picture for energy investors, where immediate reactions are swiftly counterbalanced by enduring uncertainties.

Market Volatility: From Plunge to Robust Rebound

The initial news of Hormuz’s reopening sent shockwaves through the trading floors, with crude prices reportedly plummeting more than 9% on the prospect of restored supply volumes. This sharp downturn aligned with the recent bearish trend observed over the past two weeks, where Brent crude had shed approximately 7%, moving from $101.16 on April 1st to $94.09 on April 21st. The expectation was that an influx of previously constrained barrels would immediately ease the tight supply environment that has kept prices elevated and volatile.

However, the market’s response has proven to be anything but straightforward. As of today, Brent crude trades robustly at $101.68 per barrel, marking a significant 3.25% gain on the day, with an intraday range reaching $102.31. Similarly, WTI crude has surged to $92.73, up 3.41%, after dipping as low as $87.64 earlier. This powerful rebound, just hours after the initial price drop, suggests that while the reopening offers immediate relief, traders are quickly factoring in deeper considerations. It points to a prevailing underlying bullish sentiment, perhaps driven by lingering skepticism about the permanence of the ceasefire, persistent demand strength, or other geopolitical factors that continue to underpin global energy prices.

Geopolitical Headwinds and Investor Apprehension

While the physical reopening of Hormuz is a welcome development, the geopolitical landscape remains fraught with peril, a sentiment reflected in investor questions we’re seeing this week. Many are asking “Is WTI going up or down?” and seeking “predictions for the price of oil per barrel by end of 2026,” highlighting a pervasive uncertainty about oil’s future trajectory. The ceasefire between Israel and Hezbollah, the catalyst for this reopening, is delicate and subject to rapid shifts. The announcement by Iranian Foreign Minister Abbas Araghchi confirms the “completely open” status, yet the broader negotiations between the U.S. and Iran over nuclear policy, sanctions relief, and maritime security continue to be complex and protracted.

The U.S. has maintained a firm stance on Iranian exports, employing recent enforcement actions and a visible naval presence in the region. Warnings that military operations could resume if diplomatic efforts falter cast a long shadow over the stability of shipping flows through the strait. This ongoing pressure, coupled with the inherent fragility of regional ceasefires, suggests that the market may view the current situation as a temporary respite rather than a definitive resolution to supply risks. Investors must remain vigilant, as any re-escalation could quickly reverse the current optimism and plunge prices back into volatility.

Forward Outlook: Key Events Shaping the Next Fortnight

For investors navigating this complex environment, the next two weeks will be crucial, offering several key data releases that will shape market sentiment and potentially address some of the pressing questions about oil’s future. Tomorrow, April 22nd, the EIA Weekly Petroleum Status Report will provide fresh insights into U.S. crude inventories, refinery utilization, and product demand. Any unexpected drawdowns or increases in U.S. crude stockpiles could either reinforce the current bullish rebound or signal renewed downward pressure.

Following this, the Baker Hughes Rig Count on April 24th will offer an indicator of North American drilling activity, providing clues about future domestic supply expansion. Another API Weekly Crude Inventory report on April 28th and the subsequent EIA Weekly Petroleum Status Report on April 29th will continue to paint a picture of U.S. supply-demand balances. However, perhaps the most significant event for long-term investors, particularly those asking about the “price of oil per barrel by end of 2026,” will be the EIA Short-Term Energy Outlook on May 2nd. This report will offer crucial projections for global supply, demand, and price trends, providing much-needed clarity amidst the geopolitical flux and the evolving situation in the Strait of Hormuz. These upcoming data points, combined with continued monitoring of regional stability, will be instrumental in determining if the market’s initial relief translates into sustained stability or merely precedes another phase of volatility.