The energy investment landscape is currently characterized by a fascinating dichotomy, presenting both challenges and compelling opportunities for discerning investors. While traditional oil and gas markets navigate geopolitical shifts and supply-demand intricacies, the clean energy sector is undergoing a significant re-evaluation, driven by technological breakthroughs and evolving policy frameworks. Recent market movements, amplified by proprietary data insights, paint a picture where specific clean power segments are experiencing secular demand growth, particularly those tied to the burgeoning artificial intelligence infrastructure, even as other renewable sub-sectors grapple with policy-induced headwinds. Concurrently, the crude complex continues its dance with volatility, influenced by macro events and critical upcoming supply-side decisions. Understanding these divergent forces is paramount for strategic capital allocation in today’s dynamic energy portfolio.

AI Infrastructure Ignites a New Clean Power Era

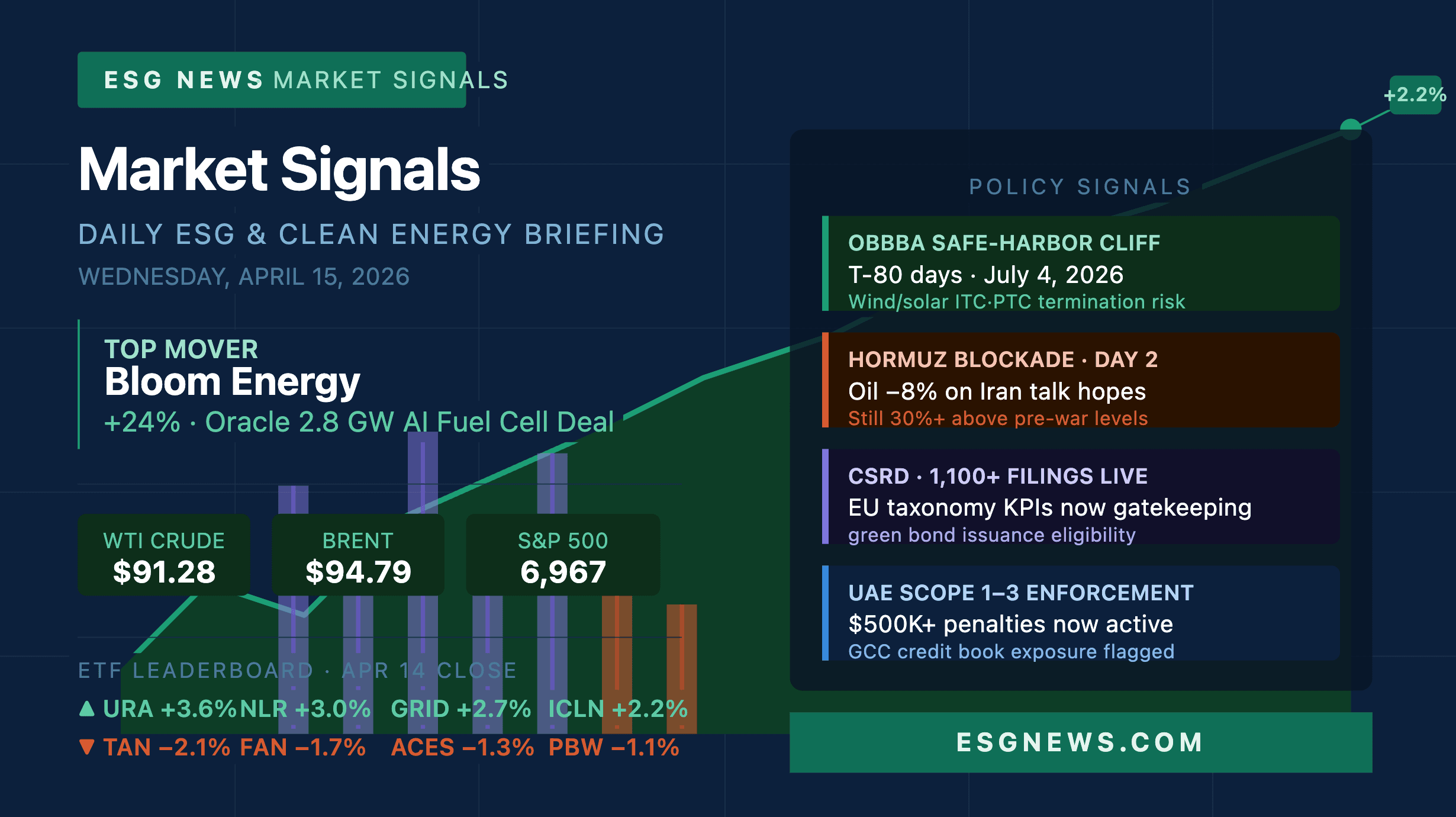

Recent sessions have underscored the emergence of AI infrastructure as a powerful catalyst for specific clean energy segments. A landmark deal, involving Oracle’s commitment to 2.8 GW of fuel-cell capacity from Bloom Energy, sent ripples across the market, driving Bloom’s shares up approximately 24% in a single day. This agreement, which includes 1.2 GW already underway for U.S. AI and cloud data centers, firmly cements “behind-the-meter” power generation as a core requirement for hyperscale computing. Investment banks like Jefferies have responded with upgrades, and JPMorgan has notably raised its price target for Bloom Energy to $231, recognizing this as the largest direct hyperscaler power commitment in fuel cell history.

This development validates the “Bring Your Own Power” thesis, propelling the entire distributed-generation basket higher. Our proprietary data confirms this momentum, with ETFs like the SPDR S&P Kensho Clean Power ETF (CNRG) leading performers, posting gains of +4.1%. Similarly, the Global X Uranium ETF (URA) and VanEck Uranium & Nuclear ETF (NLR) extended their 2026 outperformance, rising +3.6% and +3.0% respectively, reflecting a broader recognition of nuclear’s role in stable, carbon-free baseload power for energy-intensive applications. The First Trust Nasdaq Smart Grid Infrastructure ETF (GRID) also saw significant upside, up +2.7%, as the need for robust and intelligent grid solutions to support this distributed generation becomes increasingly critical. Investors are keenly observing how these AI-driven power demands will reshape long-term energy infrastructure, seeking clarity on the sustainability of this growth trajectory and the potential for further price re-ratings across the value chain.

Oil Market Volatility Persists Amidst Critical Upcoming Events

While clean energy carves out new demand niches, the traditional oil market remains a crucible of volatility, demanding constant vigilance from investors. As of today, Brent Crude trades at $95.01 per barrel, marking a significant daily increase of +5.12%, with its day range spanning $92.77 to $97.81. WTI Crude mirrors this strength, currently at $86.92, up +5.24% today, fluctuating between $85.45 and $89.6. Gasoline prices have also climbed, reaching $3.03, a +3.41% increase within a $2.99-$3.08 range.

This recent upswing comes after a pronounced period of decline. Our 14-day Brent trend analysis reveals a sharp drop from $112.78 on March 30th to $90.38 by April 17th, representing a substantial 19.9% decrease. This prior downturn was partly influenced by renewed hopes for Iran peace talks, which briefly weighed on supply expectations. However, the market’s current rebound reflects shifting sentiment and an anticipation of upcoming supply-side decisions. Many investors are asking about the direction of WTI and broader oil prices for the remainder of 2026, a question heavily tied to the next few weeks.

The immediate horizon is packed with critical events that will undoubtedly shape market direction. On April 20th, the OPEC+ Joint Ministerial Monitoring Committee (JMMC) convenes, followed by the full OPEC+ Ministerial Meeting on April 25th. These gatherings are pivotal for assessing current market conditions and potentially adjusting production quotas. Any deviation from expected policy could trigger significant price swings. Furthermore, the market will closely watch the API Weekly Crude Inventory reports on April 21st and 28th, alongside the EIA Weekly Petroleum Status Reports on April 22nd and 29th, for crucial insights into U.S. supply-demand balances. The Baker Hughes Rig Count on April 24th and May 1st will also provide a barometer for future domestic production activity. These events collectively represent a concentrated period of catalysts that will determine whether the recent oil price strength can be sustained or if renewed downward pressure will emerge.

Policy Headwinds Challenge Traditional Renewables, ESG ETFs Diverge

In stark contrast to the targeted growth seen in AI-adjacent clean power, the broader solar and wind sectors continue to absorb a structural policy discount. These segments, traditionally more exposed to government subsidies and incentives, are facing increasing scrutiny as a key deadline approaches. The “construction-start cliff” associated with the OBBBA, set for July 4th, is now less than 80 days away (from the perspective of the initial market signals), creating significant uncertainty for projects that haven’t broken ground. This looming deadline contributes to a challenging environment for subsidy-dependent renewable developers and projects.

Our proprietary ETF leaderboard highlights this bifurcation clearly. While nuclear and grid infrastructure ETFs surged, the Invesco Solar ETF (TAN) saw a decline of -2.1%, and the First Trust Global Wind Energy ETF (FAN) was down -1.7%. Other broader clean energy funds, such as the ALPS Clean Energy ETF (ACES) and Invesco WilderHill Clean Energy ETF (PBW), also registered losses of -1.3% and -1.1%, respectively. Even the Vanguard ESG U.S. Stock ETF (ESGV), a more diversified ESG play, closed down -0.5%. This indicates that while the overarching ESG investment theme remains strong, investors are becoming increasingly selective, differentiating between clean energy technologies with clear, market-driven demand and those heavily reliant on expiring policy support. The market is signaling a preference for robust, self-sustaining growth models over those with perceived policy risk, prompting questions from investors about the resilience of integrated energy companies in navigating both traditional and evolving clean energy landscapes.

Strategic Allocation in a Bifurcated Energy Market

The current energy investment landscape demands a nuanced approach, moving beyond broad thematic bets to focus on specific, high-conviction opportunities. We are witnessing a clear bifurcation: segments of the clean energy market, particularly those aligned with critical infrastructure like AI data centers and reliable baseload power such as nuclear, are demonstrating strong, secular demand drivers. These areas are proving less susceptible to the policy fluctuations that are currently challenging more traditional, subsidy-exposed renewable sectors like solar and wind.

For oil and gas investors, this environment underscores the importance of actively managing exposure. While the recent rebound in crude prices offers some relief, the underlying volatility, driven by geopolitical tensions and OPEC+ decisions, remains a constant. The confluence of upcoming inventory reports and crucial OPEC+ meetings in the next two weeks will be instrumental in dictating short-term price action, influencing whether current levels are sustainable or merely a temporary reprieve. Smart allocation in this climate means not only monitoring traditional energy market signals but also recognizing the emergent, market-driven demand for certain clean energy solutions. The era of a monolithic “clean energy” investment thesis is over; a granular understanding of sub-sector dynamics and policy impacts is now paramount for generating alpha in the evolving global energy mix.