Escalating Middle East Conflict Triggers Dual Maritime Risk, Threatening Global Oil Supply

The geopolitical landscape for global energy markets has undergone a significant and concerning transformation with the formal entry of Yemen’s Houthi rebels into the escalating Middle East conflict. This development establishes a potent secondary maritime flashpoint within the Red Sea, a critical area for crude and refined product transit, according to analysis by J.P. Morgan’s head of global commodities strategy, Natasha Kaneva, and her team. While the full operational ramifications of Houthi involvement continue to be assessed, their engagement fundamentally reconfigures the risk matrix, posing new challenges to global supply chains already under pressure.

The immediate and most critical implication is geographic. The conflict’s epicentre has expanded dramatically, no longer concentrated solely in the Persian Gulf and its indispensable artery, the Strait of Hormuz. Instead, it now extends into the Red Sea and, crucially, the Bab el-Mandeb strait – a globally vital chokepoint for the movement of both crude oil and refined petroleum products. The alarming reality facing investors is the simultaneous exposure of two primary corridors of global energy trade. This dual threat severely limits viable rerouting options for tanker traffic, thereby substantially amplifying system-wide supply-chain fragility and prompting a comprehensive reassessment of logistical resilience within the sector.

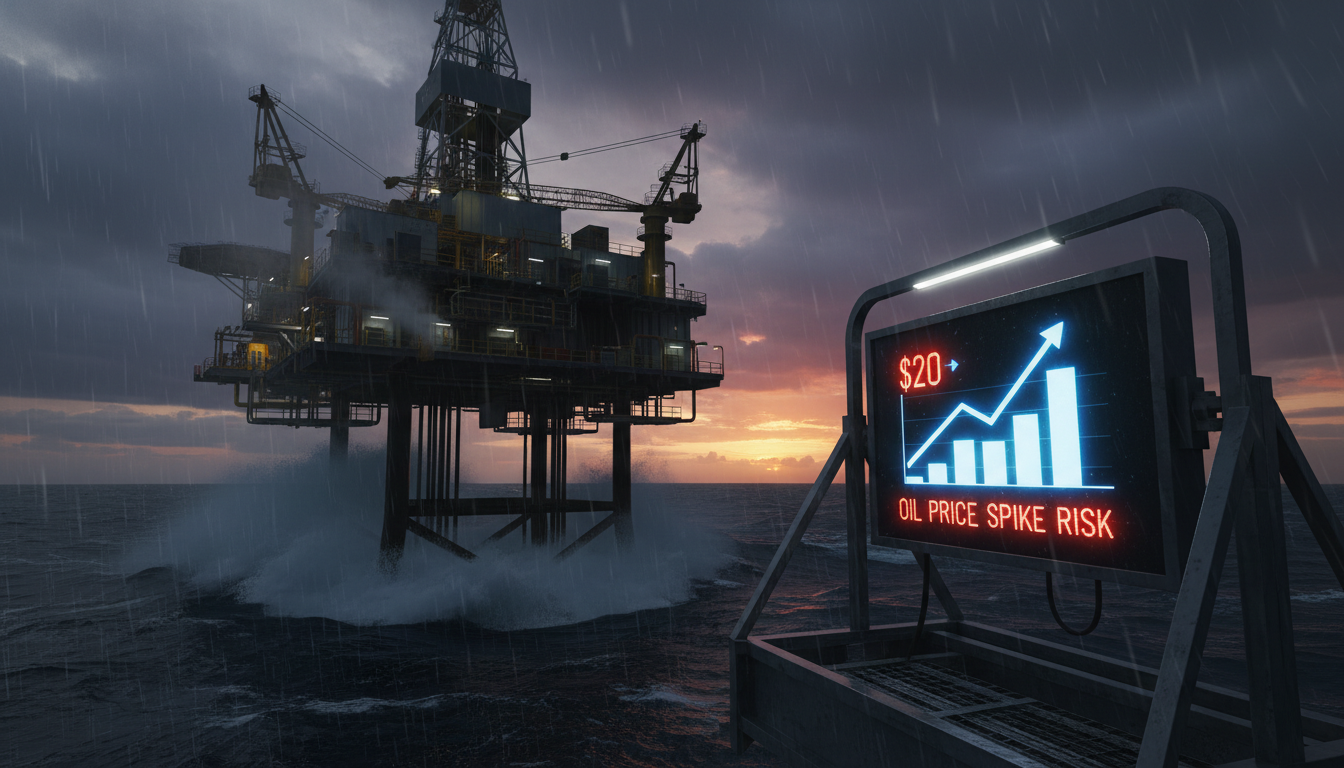

From an operational perspective, the Houthis’ participation grants them significant leverage, primarily through their capacity to menace Saudi Arabia’s strategic Yanbu export hub located on the Red Sea. Furthermore, their actions directly threaten commercial shipping traversing the Bab el-Mandeb strait, which guards the Red Sea’s southern entrance. Even smaller yet strategically important facilities, such as the Saudi Rabigh port, responsible for approximately 200,000 barrels per day of oil product exports, now face potential disruption. Cumulatively, these mounting risks could severely compromise Riyadh’s critical ability to bypass the Strait of Hormuz for a portion of its oil exports – an option vital for ensuring global supply stability during periods of heightened tension.

The tangible economic consequences of this vulnerability are profound. Approximately five million barrels per day of Saudi bypass capacity, currently routed through the Yanbu facility, now stand directly exposed to potential interruption. Such a significant impairment to supply could, by current expert estimates, translate into an immediate surge of $20 per barrel in global crude oil prices. This scenario underscores the acute sensitivity of energy markets to even perceived threats against major supply channels, demanding close attention from institutional and retail investors alike.

Crude Prices Surge Amid Conflict’s Fifth Week, Broader Economic Warning Signals

As the Middle East conflict enters its fifth tumultuous week, market participants continue to grapple with a barrage of conflicting signals. Aaron Hill, chief market analyst at FP Markets, recently articulated this sentiment, highlighting the persistent challenges. The Strait of Hormuz, a pivotal waterway responsible for a fifth of the world’s seaborne oil trade, continues to face severe transit impediments, while consumers observe an upward trend in gasoline pump prices. Despite various attempts at de-escalation towards the end of last week, energy prices largely maintained their upward trajectory, signaling underlying market strength.

Brent Crude spot prices closed robustly above the $100 per barrel threshold last Friday, registering an impressive 6.2 percent gain to settle at $106.30. Similarly, West Texas Intermediate (WTI) spot prices, after recovering significantly from earlier lows, pushed back over $100, closing the week at $101.17. This demonstrated resilience in crude prices indicates a deeper structural shift rather than mere speculative fervor, pointing to genuine supply concerns that transcend daily headlines.

The sustained elevation of crude oil prices presents a significant headwind for broader equity markets. Hill astutely observes that persistently high energy costs effectively act as an economy-wide tax, impacting nearly every facet of commercial and consumer activity. Equity valuations are already beginning to reflect this drag, underscoring the critical interplay between energy commodity prices and overall economic health. Investors must brace for potential volatility as these higher input costs ripple through corporate earnings and consumer spending patterns.

Energy Markets Undergo ‘Regime Shift’ from Risk Premium to Physical Shortage

Saxo Bank’s head of commodity strategy, Ole Hansen, recently articulated a critical paradigm shift occurring within energy markets over the past month. He asserts that the market has transitioned from merely pricing in a geopolitical risk premium to actively grappling with a tangible physical supply shock. This profound change is primarily propelled by the effective disruption of oil flows through the Strait of Hormuz, forcing a fundamental re-evaluation of global supply security and pricing mechanisms across the entire energy complex.

A particularly urgent development, as highlighted by Hansen, is the rapid depletion of “oil on water.” This refers to the volume of crude and products currently in transit on tankers globally, which often acts as a critical buffer against immediate supply disruptions. Tankers that departed the Arabian Gulf before the recent escalation have now largely reached their destinations and offloaded their precious cargoes. With a constrained flow of new supply entering the market from the region, this crucial cushioning effect that initially absorbed and mitigated sharp price spikes is quickly diminishing, leaving markets far more exposed to immediate supply-side pressures and price volatility.

Concurrently, the necessary rerouting of numerous vessels around the longer, more arduous Cape of Good Hope journey has dramatically extended shipping times and imposed substantial increases in logistical costs. This diversion directly impacts the prompt availability of both crude oil and its refined derivatives across key global consumption hubs. This tightening of physical supply is starkly evident in the robust performance of diesel and jet fuel markets, where prices continue to command a significant premium over crude. This divergence serves as a powerful indicator that the market is definitively moving beyond mere futures-driven risk repricing, instead confronting a genuine physical shortage dynamic. Investors should closely monitor these refined product markets as a leading indicator of broader energy market stress and a bellwether for potential economic slowdowns.