The United Kingdom’s latest carbon storage licensing round presents a pivotal opportunity for investors in the evolving energy landscape, signaling a clear strategic direction for the nation’s energy transition. This new initiative, offering investment areas across two distinct categories, underscores a robust commitment to decarbonization while leveraging existing hydrocarbon infrastructure and geological advantages. For oil and gas companies, both established giants and innovative startups, these opportunities are not merely about environmental compliance but represent a significant avenue for diversification, long-term revenue streams, and strategic positioning in the burgeoning carbon capture and storage (CCS) market. Understanding the nuances of these offerings, the market context, and the regulatory framework is crucial for any investor looking to capitalize on the UK’s ambitious net-zero targets.

Strategic Tiers Define New CCS Opportunities

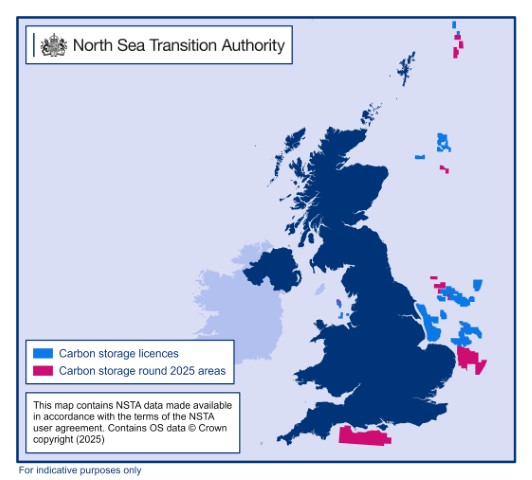

The North Sea Transition Authority (NSTA) has unveiled a new set of carbon storage areas, categorizing them into two strategic tiers designed to optimize project delivery and investor interest. The first tier comprises depleted hydrocarbon fields, carefully selected by the NSTA. These sites offer inherent advantages, including existing geological data, potential for repurposing infrastructure, and a proven understanding of subsurface conditions, which can significantly de-risk project development. The second tier focuses on saline aquifer sites, identified through a proactive “Call for Nominations” that allowed industry partners to propose areas with high potential for successful project execution. This industry-led input ensures that the allocated sites align with commercial viability and technological readiness.

These 14 new areas, with five situated in Scottish waters and nine off the coast of England, are the result of extensive consultations with key stakeholders, including The Crown Estate and Crown Estate Scotland. This collaborative approach highlights the integrated effort required to advance CCS projects. Successful applicants will need to secure a carbon storage license from the NSTA, followed by a crucial seabed agreement from the respective Crown Estate body, before commencing operations. This multi-stage process, while rigorous, aims to ensure environmental integrity and coordinated development. The application window for this licensing round extends until Tuesday, March 24, 2026, with licenses anticipated to be awarded in early 2027, establishing a clear, albeit long-term, investment horizon.

Navigating Volatility: CCS as a Diversification Play

In a market characterized by pronounced volatility, investments in stable, long-term energy transition projects like CCS gain significant appeal. As of today, Brent crude trades at $91.87, reflecting a notable daily downturn of 7.57% and a wide intraday range between $86.08 and $98.97. Similarly, WTI crude has seen a substantial drop of 7.86% to $84, fluctuating within a daily range of $78.97 to $90.34. This immediate market sentiment follows a broader trend; our proprietary data shows Brent crude declining from $112.57 on March 27th to $98.57 by April 16th, representing a 12.4% decrease in just over two weeks. Even gasoline prices have dipped, currently at $2.95, down 4.85% today. This persistent price instability underscores the challenges and uncertainties inherent in traditional hydrocarbon markets.

Against this backdrop, the UK’s commitment to CCS offers a compelling diversification strategy. While our proprietary reader intent data reveals significant investor focus on short-term market movements, such as the performance of major players or predictions for oil prices by the end of 2026, CCS projects represent a deliberate shift towards de-risked, government-backed growth. The UK government’s commitment of up to £21.7 billion for these initiatives provides a strong financial underpinning, projecting a contribution of approximately £5 billion per year of gross value added (GVA) to the UK economy by 2050 and the creation of 50,000 long-term jobs. For energy companies looking to hedge against crude price swings and future demand uncertainties, investing in CCS provides a pathway to sustained revenue and strategic relevance in a decarbonizing world.

Milestones and Regulatory Coordination: A Forward Look

The timeline for this new licensing round, with applications closing in March 2026 and awards in early 2027, demands a long-term strategic view from investors. This contrasts sharply with the immediate market attention on events like the upcoming OPEC+ Joint Ministerial Monitoring Committee (JMMC) meeting tomorrow, April 17th, and the full Ministerial Meeting on April 18th, which often dictate short-term price movements. Similarly, weekly data releases such as the API Crude Inventory on April 21st and 28th, and the EIA Weekly Petroleum Status Reports on April 22nd and 29th, provide crucial short-term insights into supply-demand dynamics. While these events are critical for tactical trading, CCS investments align with a much broader, multi-year energy transition narrative.

The UK has already laid significant groundwork, with the first carbon storage licensing round in September 2023 resulting in 21 awarded licenses. Further progress was seen with the NSTA awarding the first storage permits to two flagship projects: Endurance and HyNet. The Endurance site off Teesside, capable of storing up to 100 million tonnes of CO2, received its permit in December 2024. The Liverpool Bay-based HyNet project, also targeting 100 million tonnes of CO2 storage over 25 years, secured three permits in April 2025. These successful precedents demonstrate the viability and the progressive nature of the UK’s CCS framework. The ongoing collaboration between the NSTA, The Crown Estate, and Crown Estate Scotland to streamline licensing and leasing approaches is a positive sign for developers, promising a more efficient application process in future rounds.

Investor Focus: Beyond Hydrocarbons

Our analytics consistently show that investors are grappling with fundamental questions about the future of energy, exemplified by queries regarding future oil price predictions and the production quotas of OPEC+. There’s a clear appetite for understanding how traditional oil and gas companies, such as Repsol, are positioning themselves in this evolving environment. The UK’s new CCS licensing round provides a concrete answer to these strategic concerns for integrated energy companies. By offering a structured pathway into carbon capture and storage, these opportunities allow companies to pivot towards a lower-carbon future, leveraging their existing expertise in subsurface geology, project management, and large-scale infrastructure development.

Investing in these new areas is not just about environmental responsibility; it’s about securing future growth in ‘hard-to-abate’ industrial sectors that require decarbonization solutions. These projects provide a tangible mechanism for established oil and gas players to transition their business models, reduce their carbon footprint, and maintain relevance in a global economy increasingly focused on net-zero targets. The long-term nature of these investments, coupled with significant government support and a clear regulatory framework, positions them as attractive assets for institutional investors and energy majors seeking sustainable growth beyond the immediate fluctuations of crude markets.