India, a colossal energy consumer, is currently at the epicenter of a significant reordering of global crude oil flows. With stringent sanctions on major Russian producers, including Rosneft PJSC and Lukoil PJSC, set to fully take effect this week on November 21, the South Asian nation is aggressively pivoting its procurement strategy. This shift is not merely a tweak but a fundamental realignment, signaling profound implications for Middle Eastern producers, global shipping markets, and the broader crude price landscape. Our proprietary data indicates that this strategic pivot is already creating palpable ripples, challenging existing supply chains and prompting investors to scrutinize the durability of current market dynamics.

India’s Urgent Pivot: Reshaping Middle East Crude Flows

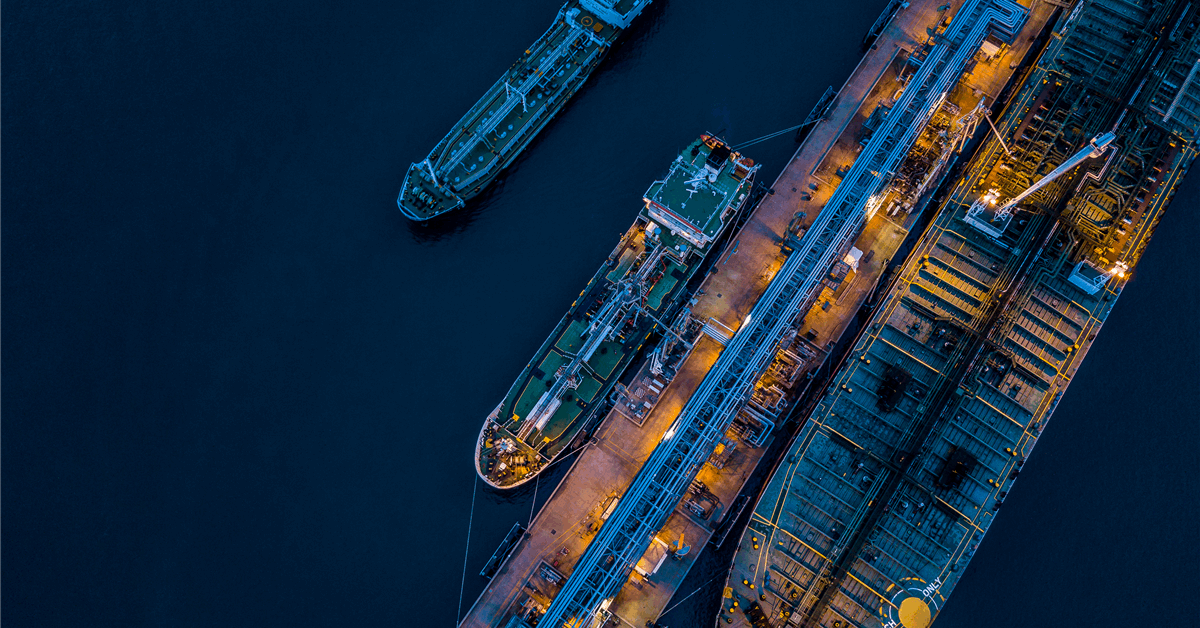

The urgency of India’s energy recalibration is strikingly evident in recent shipping activity. Our analysis of first-party shipbroker reports reveals a dramatic surge in bookings for oil tankers destined for India from key Middle Eastern producers. This week alone, roughly a dozen vessels have been chartered to transport crude from nations like Saudi Arabia, Kuwait, Iraq, and the United Arab Emirates. This marks a substantial increase from just four similar fixtures observed at the same time last month, underscoring the intensified demand. These bookings encompass a range of vessel sizes, from supertankers known as Very Large Crude Carriers (VLCCs) to the smaller, yet still significant, Suezmax vessels, all slated for oil loading between late November and December. Critically, Indian importers continue to actively seek additional tankers for these burgeoning routes, signaling that the current booking rush is far from exhaustive.

This immediate surge is a direct response to the impending cessation of Russian crude deliveries for many Indian refiners. Five of India’s seven major refiners, including industry giant Reliance Industries Ltd., have confirmed they will no longer accept Russian crude once the wind-down period concludes this week. The remaining refiners are expected to limit their purchases to non-sanctioned sellers, further tightening the pool of available supply. While India’s monthly tender volumes have shown a modest increase, traders participating in these tenders indicate that the additional supply is not yet sufficient to offset the potential loss of over one million barrels a day of Russian flows. This deficit is driving Indian refiners to pursue a dual strategy: securing more long-term supplies from Middle Eastern producers and making opportunistic spot purchases, such as prompt Kuwaiti crude made available by an unplanned outage at the Al-Zour refinery.

Freight Rates Soar Amidst Geopolitical Realignments

The concentrated demand for Middle Eastern crude, coupled with the necessity for rapid logistical adjustments, is having an immediate and pronounced impact on global shipping markets. The daily costs of hiring an oil supertanker for routes from the Middle East to Asia are now hovering near a five-year high. This escalation in freight rates directly impacts the landed cost of crude for Indian refiners, potentially squeezing their margins or necessitating price adjustments for refined products in the domestic market. For investors, this trend highlights the interconnectedness of geopolitical events, commodity flows, and logistical infrastructure. Companies involved in tanker ownership and operations are seeing an immediate boost, while refiners are facing increased operational expenditures. The sustained high demand for Middle East-to-India routes suggests that these elevated freight costs are unlikely to dissipate quickly, as the structural shift in India’s sourcing strategy appears to be a long-term development rather than a temporary anomaly.

Navigating Market Volatility: Investor Concerns and Crude Price Dynamics

Against the backdrop of India’s localized crude demand surge, the broader energy market exhibits significant volatility. As of today, Brent crude trades at $90.71 per barrel, marking an 8.73% decline within the day, with prices fluctuating between $86.08 and $98.97. Similarly, WTI crude stands at $82.9, down 9.07%, having traded within a range of $78.97 to $90.34. This intraday volatility underscores a broader market unease. Over the past 14 days, Brent crude has seen a notable decline of $14, or 12.4%, from $112.57 on March 27 to $98.57 yesterday. This broader market weakness, driven by factors such as global demand concerns and macroeconomic headwinds, contrasts sharply with the specific, intense demand for Middle Eastern crude from India.

Our proprietary reader intent data reveals that investors are keenly focused on the future trajectory of crude prices, with a recurring question being, “What do you predict the price of oil per barrel will be by end of 2026?” This question reflects a desire to understand how these conflicting signals—localized demand surges versus broader market softness—will ultimately balance out. While India’s increased Middle East imports provide a demand floor, the overall market is influenced by numerous other variables. The interplay between India’s strategic sourcing, OPEC+ production policies, and global economic health will dictate price action. Investors should note that while specific regional demand can drive up certain components like freight, the overall crude price remains susceptible to a wider array of supply-demand fundamentals.

The Supply Gap and Strategic Sourcing: Looking Ahead

The potential shortfall of over one million barrels a day of Russian crude for India creates a substantial supply gap that Middle Eastern producers are now scrambling to fill. This reallocation is a strategic boon for countries like Saudi Arabia, Kuwait, Iraq, and the UAE, solidifying their position as pivotal global energy suppliers. The shift underscores the critical importance of supply diversity for major importers like India and highlights the geopolitical risks inherent in relying too heavily on any single source.

Looking forward, critical upcoming events will further shape the energy landscape. The OPEC+ Joint Ministerial Monitoring Committee (JMMC) meeting today, April 17, followed by the Full Ministerial meeting tomorrow, April 18, will be closely watched by investors. Readers are specifically asking, “What are OPEC+ current production quotas?” The outcome of these meetings, particularly any decisions regarding production levels, will directly impact the availability and pricing of the very Middle Eastern crude that India is so aggressively seeking. Any decision to maintain or adjust current quotas will immediately influence global crude balances and, by extension, India’s sourcing costs and strategic options. Further insights into supply and demand dynamics will come from the API Weekly Crude Inventory reports on April 21 and 28, and the EIA Weekly Petroleum Status Reports on April 22 and 29, which will provide fresh data on US crude stockpiles and refinery activity. These reports, alongside the Baker Hughes Rig Count on April 24 and May 1, will offer a clearer picture of the broader supply-side response to global energy shifts. For investors, monitoring these data points and the ongoing geopolitical shifts is paramount to understanding the future trajectory of the oil and gas market.