The EV Battery Revolution and its Impact on Oil Demand Dynamics

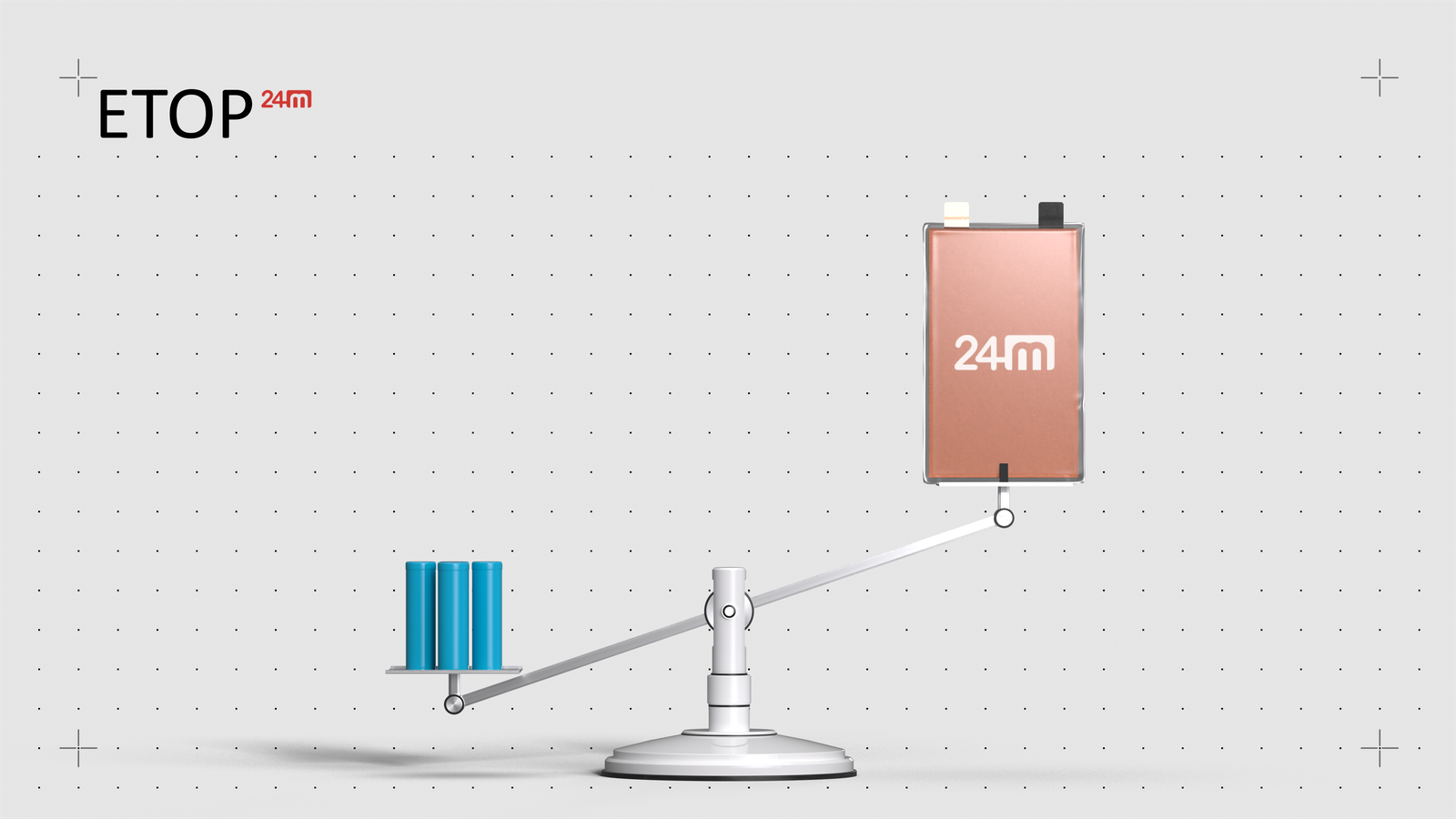

A recent breakthrough in battery technology promises to fundamentally reshape the electric vehicle (EV) landscape, with significant implications for the oil and gas sector. A pioneering technology company has unveiled a new battery packing system, dubbed ETOP, which boasts unmatched energy density. This innovation could boost EV driving range by up to 50% or drastically reduce manufacturing costs, presenting a potent challenge to gasoline demand and compelling oil investors to reassess long-term outlooks. By eliminating inactive materials and integrating electrodes directly into the pack, ETOP allows electrodes to comprise an unprecedented 80% of a battery pack’s volume, a substantial leap from the 30% to 60% seen in traditional designs. This efficiency gain means car manufacturers can either offer consumers extended ranges – for example, increasing a 75kWh NMC battery to over 100kWh within the same physical footprint – or achieve comparable ranges using less expensive chemistries like LFP, thereby driving down EV sticker prices. Such advancements accelerate EV adoption, directly eroding the market share of internal combustion engine vehicles and, by extension, global oil demand.

Current Market Pressures and the Shadow of Future Demand Erosion

The potential for long-term demand erosion from EV advancements is juxtaposed against immediate market volatility. As of today, Brent crude trades at $90.38 per barrel, marking a significant 9.07% decline from its opening. Similarly, WTI crude has fallen to $82.59, down 9.41% within the day’s trading range. Gasoline prices have also seen a notable dip, currently at $2.93 per gallon, a 5.18% decrease. This recent dip is not an isolated event; our proprietary pipelines show Brent has shed $20.91, or 18.5%, from its March 30th peak of $112.78. While current price movements are influenced by a confluence of geopolitical factors, macroeconomic concerns, and inventory levels, the underlying sentiment is increasingly sensitive to narratives of future demand uncertainty. The rapid evolution of EV battery technology, as exemplified by the ETOP system’s promise of greater range and lower cost, adds another layer of long-term bearish pressure that astute oil and gas investors cannot ignore. These developments suggest that even short-term price rebounds may face structural headwinds as the energy transition gains momentum.

Navigating Upcoming Catalysts: OPEC+ and Inventory Dynamics

While technological innovation reshapes the distant horizon, oil and gas investors must also closely monitor near-term market catalysts. Our event calendar highlights several critical dates in the coming fortnight that will provide further clarity on supply-demand dynamics. With Brent trading significantly lower than recent highs, all eyes will be on the OPEC+ Joint Ministerial Monitoring Committee (JMMC) meeting on April 18th, followed by the Full Ministerial Meeting on April 19th. These gatherings are crucial as the cartel evaluates market conditions and potentially adjusts production quotas. Investors are actively asking about current OPEC+ production quotas, and these meetings will determine if the group maintains, cuts, or even cautiously increases supply in response to recent price weakness and the broader demand outlook. Furthermore, weekly crude inventory data from API (April 21st, April 28th) and the EIA’s Petroleum Status Reports (April 22nd, April 29th) will offer vital insights into real-time supply-demand balances. Any unexpected builds or draws could trigger immediate price reactions. Finally, the Baker Hughes Rig Count on April 24th and May 1st will provide a barometer of North American upstream activity, indicating how producers are responding to current price signals and future investment outlooks. These events will shape near-term price volatility, providing tactical opportunities and risks against the backdrop of long-term energy transition pressures.

Investor Sentiment: Addressing the Long-Term Oil Price and Company Strategy

Our proprietary reader intent data reveals a consistent theme among sophisticated investors: a keen focus on the future trajectory of oil prices and the strategic responses of industry players. A dominant question is, “what do you predict the price of oil per barrel will be by end of 2026?” While precise predictions are challenging, the introduction of technologies like ETOP significantly complicates the demand side of the equation. Accelerating EV adoption, fueled by greater range and affordability, implies a peak in gasoline demand could arrive sooner than many previously anticipated, placing persistent downward pressure on long-term oil prices. This necessitates a strategic re-evaluation for integrated oil and gas companies. Investors are also inquiring about the performance of specific players, asking, “How well do you think Repsol will end in April 2026?” The performance of companies like Repsol will increasingly depend on their ability to adapt to this evolving energy landscape, diversifying into renewables, optimizing their upstream portfolios for low-cost production, and managing their refining and petrochemical assets efficiently in a world where transportation fuels face structural decline. The ability to pivot and integrate sustainable practices, alongside managing traditional assets, will be key differentiators for value creation in the coming years as the energy transition, accelerated by breakthroughs like ETOP, gains irreversible momentum.